Does Weakened Employment Spell Doom for Housing? The GSHMR for May, 2026

Welcome to the Greater Seattle Housing Market Review. As always, to skip right to the stats, you can do so by clicking here to watch the video. For much more detailed information, continue reading below.

We’ve all grown accustomed to Seattle’s economy acting like an unstoppable freight train, fueled by a decade of relentless tech wealth, soaring office demand, and eye-popping wage growth. But if you’ve been tracking the latest local economic forecasts from the city and state, it’s clear that the local engine is losing some speed.

As a data-driven observer of our local housing ecosystem, I always preach that real estate doesn't operate in a vacuum. What happens to local payrolls, tech headcounts, and municipal tax coffers eventually lands on the doorsteps of our neighborhoods.

Let’s break down the latest data points hitting the wires and, more importantly, look at what this actually means for our local housing market. There might be some similarities to last months article, "Don't Trust the Headlines".

The Macro Data: Seattle Loses Some Steam

The latest employment figures from the Washington Employment Security Department and city forecasting offices dropped a few eyebrow-raising metrics:

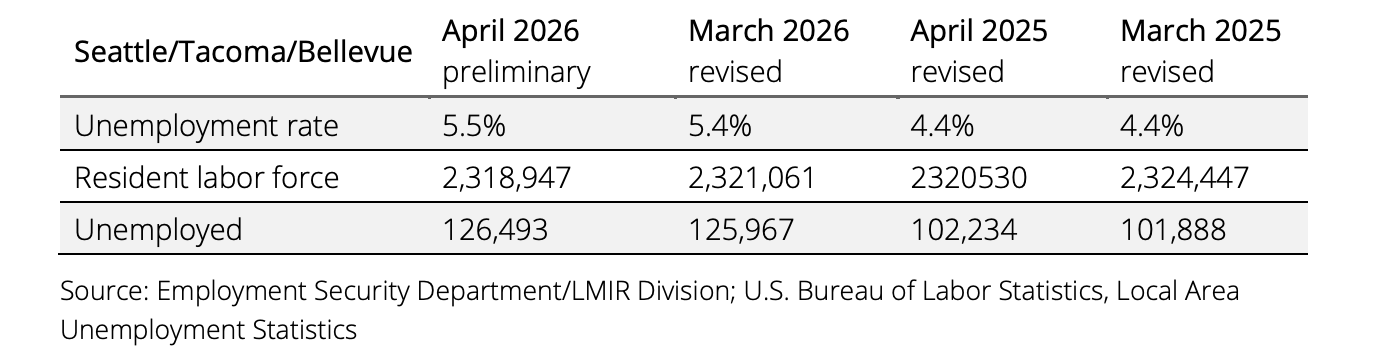

Unemployment Ticks Up: The Seattle metro area unemployment rate climbed to 5.5% in April, up from 4.4% a year earlier. For context, we are now pacing above the national average of 4.3%.

The Tech Shift: The era of tech companies hiring aggressively just to build headcount appears to be taking a backseat. Local economic updates show tech giants are heavily pivoting their capital toward AI investments and "streamlining operations." Case in point: Meta recently trimmed roughly 20% of its local Washington workforce, impacting nearly 1,400 employees.

Inflation vs. Wages: According to data from CoStar, local wage growth has slipped below inflation again. While local inflation is hovering between 4% and 5%, salary growth has cooled to under 3%.

Connecting the Dots to Residential Real Estate

When headlines shout about "warning signs" and tech layoffs, it's easy to assume the housing market is about to drop off a cliff. But real estate is rarely that linear. Here is how these economic shifts are actually playing out on the ground:

1. Incomes Squeezed, Choices Intensified

With inflation outpacing wage growth, household balance sheets are being forced to make harder decisions. Elevated home prices, driven by the massive jumps earlier in the decade combined with higher energy costs, mean buyers are naturally becoming more selective. We aren't seeing a lack of desire to buy, but we are seeing a much more calculated, price-sensitive buyer pool.

2. The Inventory Insulator

Why aren’t prices plummeting despite a cooling economy? Because structural supply remains incredibly tight. Construction activity is slowing down. Taxable sales in the construction sector fell 4.4% last year, and local construction employment shed 2,200 jobs over the past year. Less new construction means existing inventory has to carry the load, keeping a firm floor under neighborhood home values, especially in Seattle where new home construction has always been more challenging.

3. Public & Social Housing Steps In

While private commercial activity slows, we are starting to see alternative real estate sectors make massive moves. For example, Seattle Social Housing just marked its first major milestone, striking a $60 million deal to acquire a 150-unit apartment building right near Pike Place Market. Expect to see more public-private structural shifts like this as the city adjusts to lower commercial demand.

The Bottom Line

Stop listening to the bozos trying to speak a housing market crash into existence. Our area still holds its fundamental baseline advantages: an incredibly highly educated workforce, robust global tourism, and major institutional employers that anchor the Pacific Northwest.

What we are experiencing is a transition. The long-running formula of nonstop tech hiring and unchecked office demand is evolving. For buyers, this cooling momentum means a bit more breathing room and slightly less frenzied competition than the peaks of years past. For sellers, it means strategy, accurate pricing, and hyper-local presentation are more critical than ever. Markets move in cycles, and navigating the transitions is where the real opportunities are found.

Onto the stats!

(SFR)

Seattle - The median sale price registered $1,037,500. That is up YoY by 2.7% and up MoM from $999,000. Inventory is flat at just 1.7% more homes on the market YoY (yet 6.6% MORE closed sales). The months of inventory rose to 2.39 months from 2.25 in April.

Eastside - The median sale price registered $1,510,000. That is down 7.6% YoY and down from $1,612,000 MoM. Inventory remains elevated at 27.4% more homes listed YoY and the months of inventory rose to 3.7 from 3.48.

King county - The median sale price registered $975,000. That is down 1.4% YoY and up MoM from $960k.Inventory was 14.1% higher YoY while the months of inventory rose to 2.8 months from 2.5 in April.

Seattle condos - The median sale price registered $566,500. That is down 1.2% YoY and down from $575,000 MoM. Inventory is elevated, but at just 5.6% more YoY. The months of inventory rose to 5.5 months from 5 months in April.

A quick note on the condo stats. We haven't hit a months of inventory level of 5.5 or higher since September of 2024, though we've come close to it a few times. Another big milestone, May's absorption rate was the LOWEST since I've been recording these in 7+ years. As we enter the dog days of summer, I expect things to get worse for the condo market before it gets better. Gosh, I'm tired of saying that...

Enjoy the World Cup! Go Team USA! Onward!