Does Weakened Employment Spell Doom for Housing? The GSHMR for May, 2026

Welcome to the Greater Seattle Housing Market Review. As always, to skip right to the stats, you can do so by clicking here to watch the video. For much more detailed information, continue reading below.

We’ve all grown accustomed to Seattle’s economy acting like an unstoppable freight train, fueled by a decade of relentless tech wealth, soaring office demand, and eye-popping wage growth. But if you’ve been tracking the latest local economic forecasts from the city and state, it’s clear that the local engine is losing some speed.

As a data-driven observer of our local housing ecosystem, I always preach that real estate doesn't operate in a vacuum. What happens to local payrolls, tech headcounts, and municipal tax coffers eventually lands on the doorsteps of our neighborhoods.

Let’s break down the latest data points hitting the wires and, more importantly, look at what this actually means for our local housing market. There might be some similarities to last months article, "Don't Trust the Headlines".

The Macro Data: Seattle Loses Some Steam

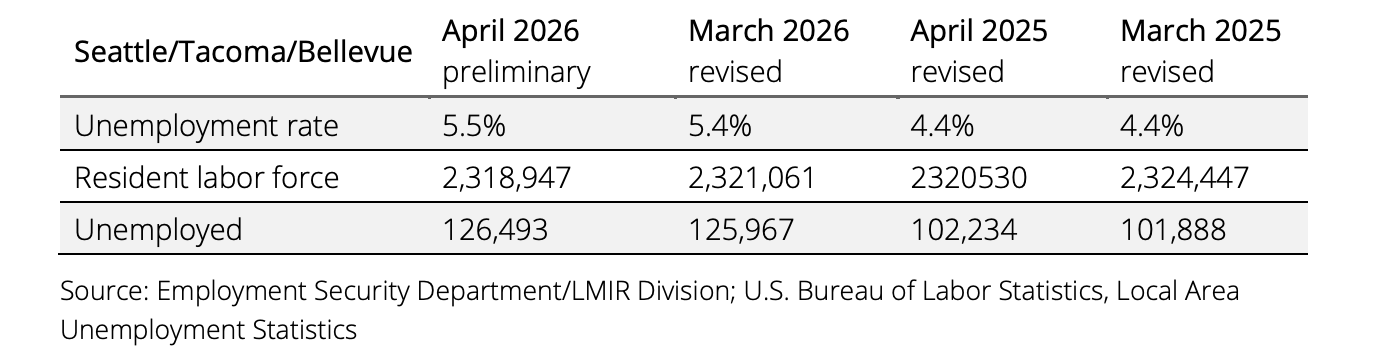

The latest employment figures from the Washington Employment Security Department and city forecasting offices dropped a few eyebrow-raising metrics:

Unemployment Ticks Up: The Seattle metro area unemployment rate climbed to 5.5% in April, up from 4.4% a year earlier. For context, we are now pacing above the national average of 4.3%.

The Tech Shift: The era of tech companies hiring aggressively just to build headcount appears to be taking a backseat. Local economic updates show tech giants are heavily pivoting their capital toward AI investments and "streamlining operations." Case in point: Meta recently trimmed roughly 20% of its local Washington workforce, impacting nearly 1,400 employees.

Inflation vs. Wages: According to data from CoStar, local wage growth has slipped below inflation again. While local inflation is hovering between 4% and 5%, salary growth has cooled to under 3%.

Connecting the Dots to Residential Real Estate

When headlines shout about "warning signs" and tech layoffs, it's easy to assume the housing market is about to drop off a cliff. But real estate is rarely that linear. Here is how these economic shifts are actually playing out on the ground:

1. Incomes Squeezed, Choices Intensified

With inflation outpacing wage growth, household balance sheets are being forced to make harder decisions. Elevated home prices, driven by the massive jumps earlier in the decade combined with higher energy costs, mean buyers are naturally becoming more selective. We aren't seeing a lack of desire to buy, but we are seeing a much more calculated, price-sensitive buyer pool.

2. The Inventory Insulator

Why aren’t prices plummeting despite a cooling economy? Because structural supply remains incredibly tight. Construction activity is slowing down. Taxable sales in the construction sector fell 4.4% last year, and local construction employment shed 2,200 jobs over the past year. Less new construction means existing inventory has to carry the load, keeping a firm floor under neighborhood home values, especially in Seattle where new home construction has always been more challenging.

3. Public & Social Housing Steps In

While private commercial activity slows, we are starting to see alternative real estate sectors make massive moves. For example, Seattle Social Housing just marked its first major milestone, striking a $60 million deal to acquire a 150-unit apartment building right near Pike Place Market. Expect to see more public-private structural shifts like this as the city adjusts to lower commercial demand.

The Bottom Line

Stop listening to the bozos trying to speak a housing market crash into existence. Our area still holds its fundamental baseline advantages: an incredibly highly educated workforce, robust global tourism, and major institutional employers that anchor the Pacific Northwest.

What we are experiencing is a transition. The long-running formula of nonstop tech hiring and unchecked office demand is evolving. For buyers, this cooling momentum means a bit more breathing room and slightly less frenzied competition than the peaks of years past. For sellers, it means strategy, accurate pricing, and hyper-local presentation are more critical than ever. Markets move in cycles, and navigating the transitions is where the real opportunities are found.

Onto the stats!

(SFR)

Seattle - The median sale price registered $1,037,500. That is up YoY by 2.7% and up MoM from $999,000. Inventory is flat at just 1.7% more homes on the market YoY (yet 6.6% MORE closed sales). The months of inventory rose to 2.39 months from 2.25 in April.

Eastside - The median sale price registered $1,510,000. That is down 7.6% YoY and down from $1,612,000 MoM. Inventory remains elevated at 27.4% more homes listed YoY and the months of inventory rose to 3.7 from 3.48.

King county - The median sale price registered $975,000. That is down 1.4% YoY and up MoM from $960k.Inventory was 14.1% higher YoY while the months of inventory rose to 2.8 months from 2.5 in April.

Seattle condos - The median sale price registered $566,500. That is down 1.2% YoY and down from $575,000 MoM. Inventory is elevated, but at just 5.6% more YoY. The months of inventory rose to 5.5 months from 5 months in April.

A quick note on the condo stats. We haven't hit a months of inventory level of 5.5 or higher since September of 2024, though we've come close to it a few times. Another big milestone, May's absorption rate was the LOWEST since I've been recording these in 7+ years. As we enter the dog days of summer, I expect things to get worse for the condo market before it gets better. Gosh, I'm tired of saying that...

Enjoy the World Cup! Go Team USA! Onward!

Don't Trust the Headlines! The GSHMR for April, 2026

Welcome to the latest edition of The Greater Seattle Housing Market Review. As always, to skip right to the video discussing last month's stats, you can do so by clicking here. For more detailed information, continue reading below.

As if legacy media wasn't already becoming increasingly untrustworthy, it's articles like this one that make gag. Those who don't know, Nick Gerill is a complete hack. He has the title "housing analyst", but the guy is nothing more than a housing doomer who has been calling for a housing market crash for years, and he's still yet to be right. Furthermore, he cowardly refuses to have debates with true housing experts who actually know what they're talking about. It's shameful our local publications bothered to pick up this pile of garbage and offer it more publicity than it deserves. Nonetheless, I digress, but not before I felt so compelled I had to offer my own $.02, here. Just another reminder to NEVER trust headlines.

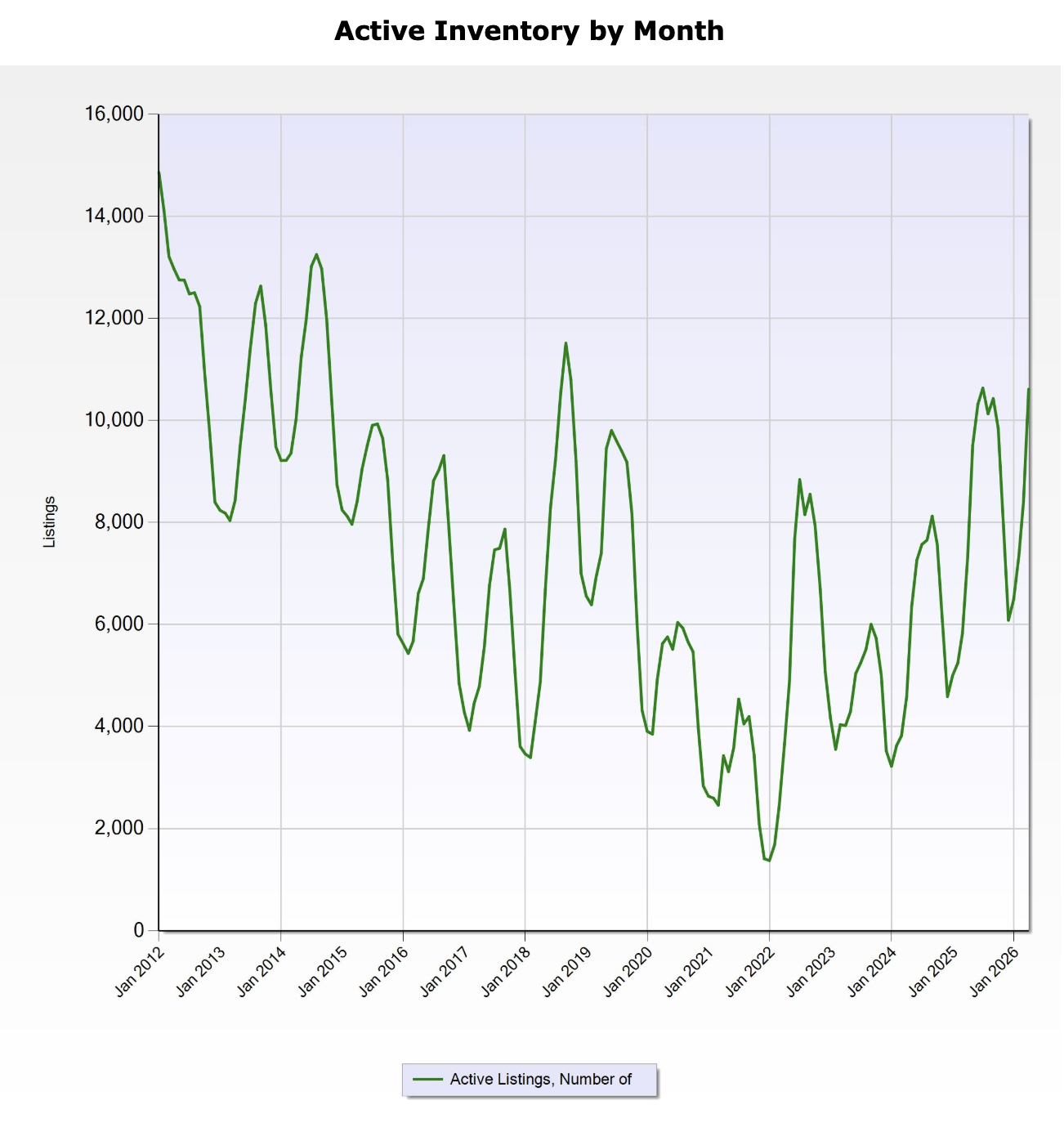

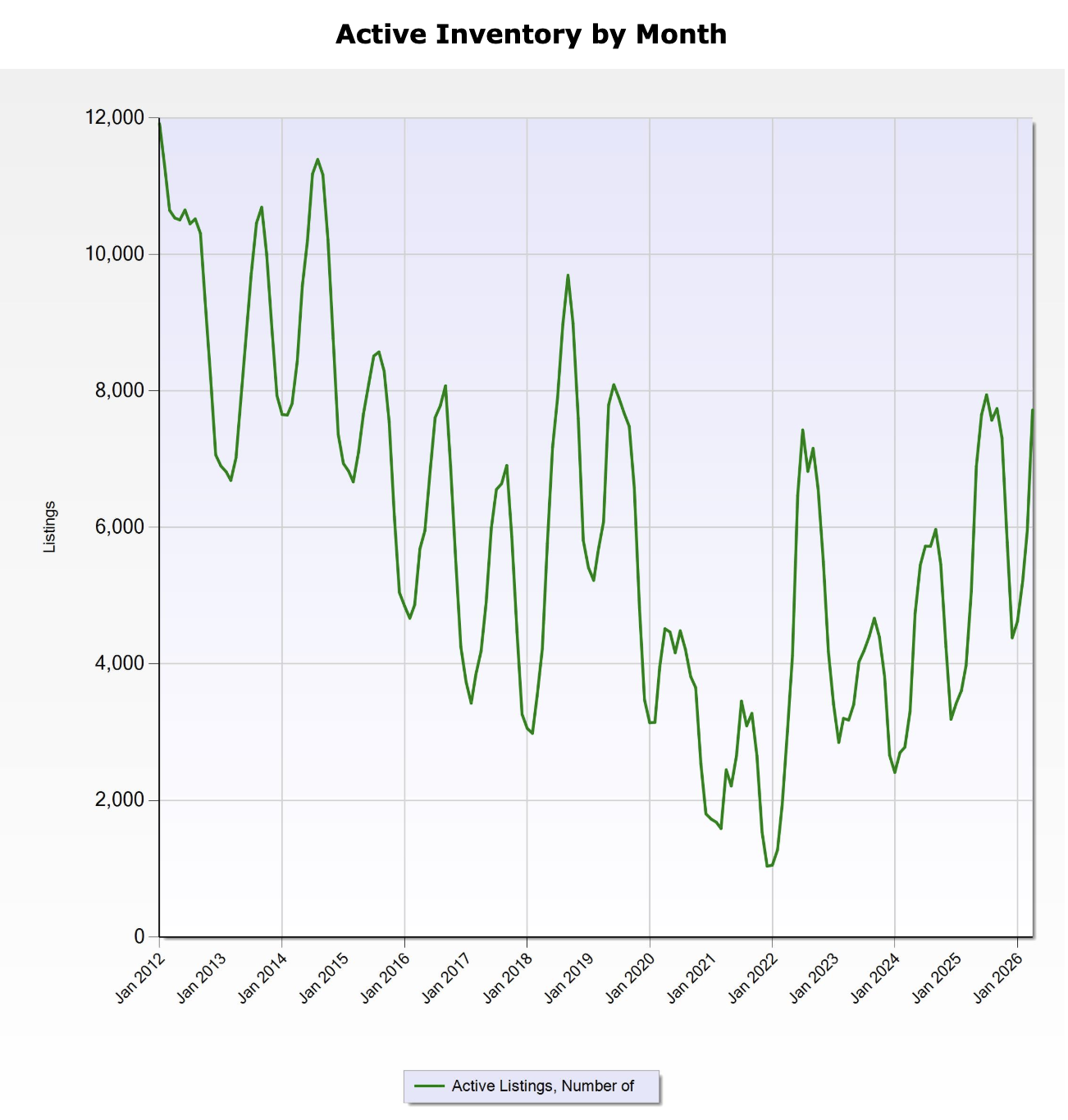

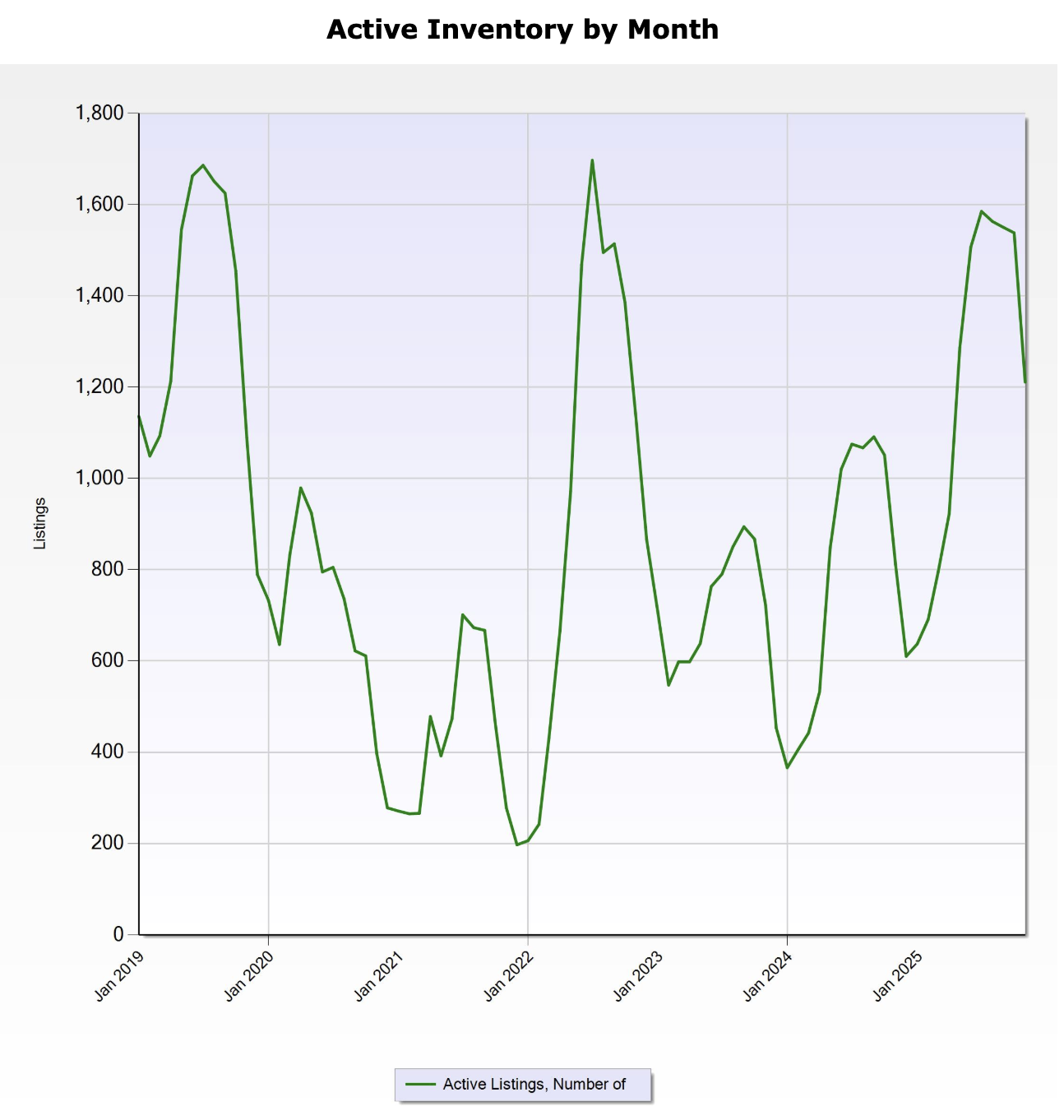

Now don't get me wrong, I'm not committing the same sin by sugarcoating everything is all sunshine and rainbows within our local housing market. The graph above is charting the total number of homes and condos for sale across King, Snohomish, and Pierce counties over the last number of years (consistent with Gerill's "reporting"). With the exception of June through September last year, we have to go back to 2018 before we've seen inventory at the level we saw last month.

Above is what the chart looks like if we remove condos from the equation. From here we see that, while we're still at relatively elevated levels of inventory, it's not the unfamiliar territory suggested by our news outlets. Granted, it was just last year, and then back in 2018 and 2019 when we saw similar levels of inventory, but this isn't some unprecedented time these unknown keyboard jockeys are trying to have you believe. What will be very interesting to watch as we get into the more listing heavy months of the year will be how inventory adds up. Especially if interest rates and affordability remain volatile. More on that below:

The following came to me courtesy of Peter Zevenbergen from NEO Home Loans. I felt it provided some very accurate context in regard to inventory and our housing market:

"This is what a normalization process looks like. We are not seeing a housing crash. We are seeing inventory slowly rebuild while price growth cools off enough for incomes and inflation to begin catching up. Think of it like a treadmill finally slowing down after being stuck at sprint speed for several years. Buyers who felt like the market was running away from them are starting to regain footing. The failed spring selling season is part of that story too. Demand has softened just enough to create breathing room without creating distress. Homes are sitting longer, negotiations are returning, and buyers have more choices than they have had in years.

The important takeaway for our clients is this; Affordability does not always improve because prices collapse. Sometimes it improves because time does the work. If inventory continues rising while home price appreciation stays muted, and if income growth continues moving higher, we could see a multi year stretch where housing becomes progressively more affordable in real terms even if nominal prices stay mostly flat. That is a very different outcome than the doom and gloom headlines many people are waiting for, and honestly, it is probably a much healthier one for the long-term stability of the housing market."

Onto the stats:

Seattle - The median sale price for a SFR in Seattle for April 2026 registered at $998,899. That is down 2.55% YoY and up MoM from $944,000. Inventory was up 27.5% YoY and the months of inventory stat rose to 2.25 months from 1.99.

Eastside - The median sale price registered at $1,612,000. That was down 5% YoY, yet up MoM from $1,550,000. Inventory was up 51.1% YoY and the months of inventory increased to 3.48 months 2.85.

King County - The median sale price registered $960,000. That is down 6.8% YoY and down MoM from $975,000. Inventory was up 36.7% YoY and the months of inventory increased to 2.5 months from 2.23 the prior month.

Enjoy the beginning of summer! Onward!

Immigration and Millennials; The GSHMR for March, 2026

And welcome to the latest edition of the Greater Seattle Housing Market Review. As always, to skip right to the stats, you can do so by clicking here. For better, and hopefully entertaining information, continue reading below.

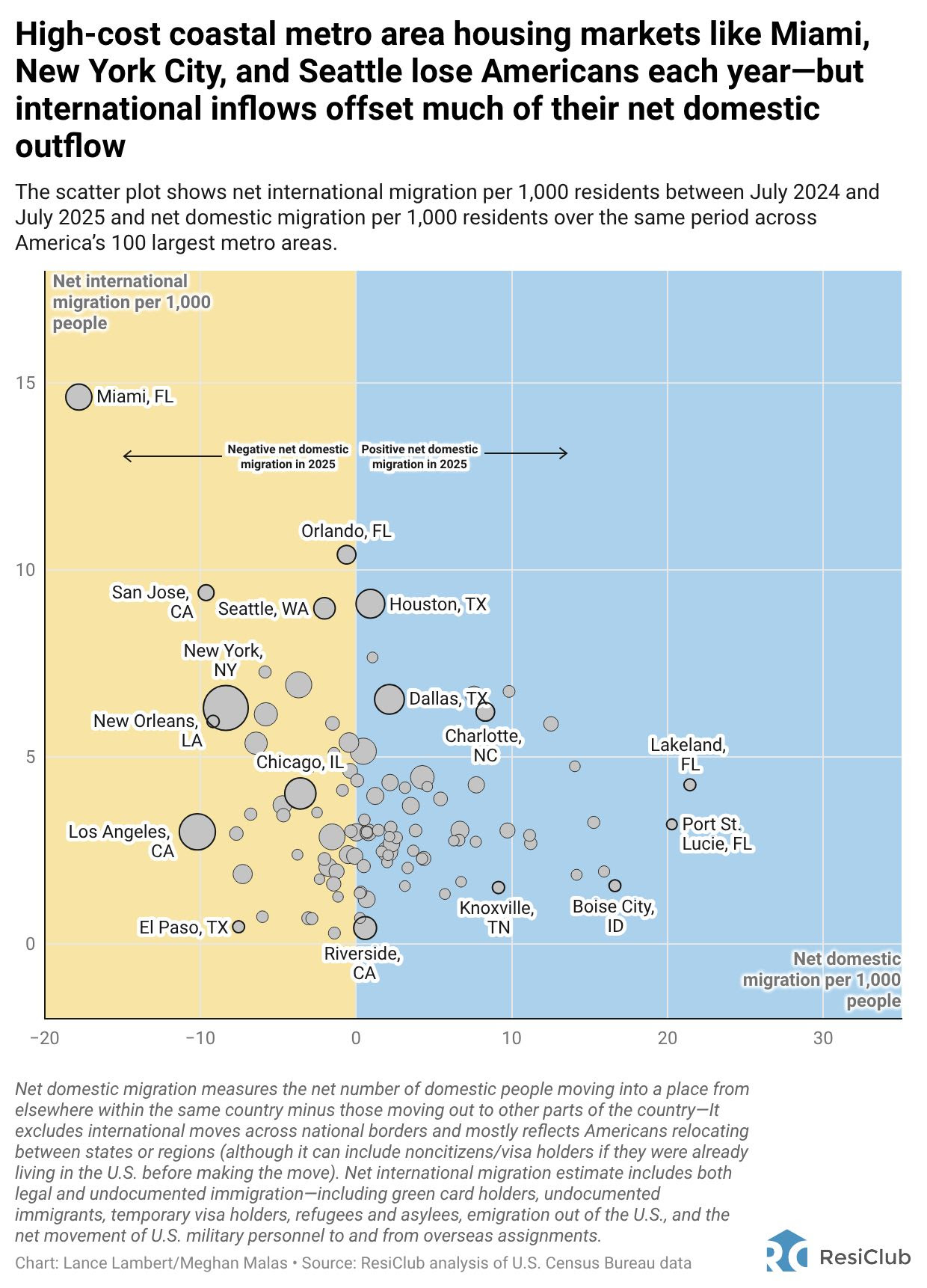

We've all heard the news, whether the reporting is fair or sensational, about Seattleites moving out of the Puget Sound region. This commentary was inspired by a recent ResiClub article that really blew my mind.

The article identified cities including Seattle, NYC, and Miami as being major metros losing American population each year, but making up for it (or getting close to it) with international immigration. See below:

To be fair, this data was collected between July 2024-July 2025 so the impacts of recent federal immigration policies might not be too visible in this data, if there has been any significant change there to begin with. To be determined. Regardless, the fact we're gaining equal or more international immigration at the expense of American emigration really blew my mind. I know we've always been an "international city" to some extent, but I wasn't thinking to that extent. This Seattle Times article touches on that.

As far as home values go, one might conclude that international immigrants replacing Americans moving into/out of Seattle would spell doom for the housing market. After all, how likely is it that someone brand new to a country can qualify to buy a home, let alone even have aspirations of doing so? Again, H1B visa drama aside, home values have been pretty flat over the past two years. Can we thank millennials?

Above is a snippet from an article from The News Tribune citing a SmartAsset poll that ranked Seattle and Bellevue as two of the top destinations for millennials. In fact, this Seattle Times article, published at the end of last year, reported that roughly one third of all Seattlites are millennials! Millennials and their strong incomes are helping to keep local home values supported, despite the exodus of American born Seattlites.

Onto the stats -

Seattle - The median sale price in March 2026 for a Seattle SFR registered $944,000. That is down 5.6% YoY and down MoM from $962,500. Inventory is up 28.6% YoY and the months of inventory statistic dropped to 1.99 months from 2.68 in February.

Eastside - The median sale price registered $1,325,000. That is down 1.23% YoY and considerably down MoM from $1,566,000. In fact, this was the lowest median sale price for the Eastside since January 2023! Inventory remains highly elevated at 60.2% more inventory YoY while the months of inventory decreased to 2.52 from 3.23.

King County - The median sale price registered $975,000. That is down just .26% YoY and up MoM from $936,000. Inventory remains elevated at 41.6% more listings YoY and the months of inventory decreased to 2.23 from 2.71 months.

That's it. Go out and have the best spring ever! We'll pick back up in May.

Onward!

Lending Changes Coming for Condos; The SCMR for March, 2026

And welcome to the latest edition of the SCMR (Seattle Condo Market Review). As always, to skip right to the stats, you can do so by watching this video. For more information on what's going on in the Seattle condo market, continue reading below!

As if I haven't been enough of a broken record over the past years detailing the struggling Seattle condo market, changes in agency lending are on the horizon that could bring additional despair. But before that, there are some positives. See below.

First, a shout out to Kyle Bergquist of Cross Country Mortgage who put these bullet point changes together in an easy to understand format.

Fannie Mae announced a few “minor” changes to their condo approval guidelines. Turns out, these could have a giant impact on the condo market. Check it out:

· Condo projects with 10 or fewer units may qualify for a review waiver (so long as they’re not part of a master association or larger development) – Verdict: Positive, but likely little to no impact. Under previous rules, condo projects with 4 or fewer units already qualified for this same waiver… So we’re really just expanding this guideline to cover the condo projects that have between 5 and 10 units, which does not greatly expand the waiver in practice (since there aren’t many additional condo projects that are now included in this guideline). Very few projects in our area are this small to begin with.

· There is no longer a 50% investor cap – Positive, but likely little to no impact. As long as a condo buyer was putting more than 10% down and purchasing the condo as their primary residence, this guideline didn’t apply under the previous Fannie Mae condo guidelines anyway. Therefore, just like the first update, great that they’re getting rid of the cap, but in our experience lending on condos in our area, this cap was rarely a failure-point for condo approval in the first place.

· Elimination of limited review for larger condo projects – Unideal and potentially hazardous. Under current guidelines, as long as a condo buyer was putting 10% or more down and buying the condo as a primary residence, they would qualify for a “Limited Review”. This meant that condo balance sheets and financials weren’t scrutinized and lenders didn't need to worry about the 50% investor cap. Eliminating the limited review opens up a lot of failure points in the condo approval process, especially because many HOAs don’t prioritize balancing their books and ensuring they remain within Fannie Mae approval guidelines. This could open up a can of worms that might not have been a problem under current and past guidelines.

· Condo Reserve Requirement increases to 15% (from 10%) - Very Unideal and potentially hazardous. The condo reserve requirement currently only applies to buyers putting less than 10% down. Now this requirement will apply to all condo buyers, regardless of down payment. The issue here is two-fold: In my experience, many condo associations had a tough time meeting the 10% reserve requirement to begin with. So, to graduate from a requirement that HOAs were already having a tough time of meeting, and requiring them to increase their reserves by 50% of the previous minimum by January 4th, 2027? I’m not sure how HOAs are going to be able to accommodate this rule change without increasing dues or levying an assessment. As if financial solvency wasn't already an issue for some buildings, the requirement now just got tougher!

· Lenders must now rely on the highest recommended reserve amount in the study – Not Ideal and potentially VERY hazardous. Under current guidelines, Fannie Mae only required a 10% reserve. Under these new guidelines, if a reserve study is conducted and it states something like “Based on the budget, the minimum reserves should be X dollars, but with pending roof, siding, and window replacements, we recommend the reserve minimum to be Y dollars…” Lenders are going to be required to go with the higher number even if the lower number meets the new 15% reserve percentage guideline. Said another way, a 15% reserve fund is the minimum. The actual required reserve amount could be higher dependent on what the reserve study states. This could be completely disastrous for any buildings with capital projects on the horizon.

· Increased allowable insurance deductible to $50,000 per unit, and the use of “Actual Cash Value” instead of full replacement cost for HOA master insurance policy coverage – Not Ideal. This is a classic short term profit for long term loss paradox. The guideline update will save condo owners money on their insurance coverage now, but if something happens and a claim needs to be filed in the future, insurance coverage is almost guaranteed to not cover the replacement cost of whatever was damaged. This could result in higher HOA dues to cover the difference, or a large one-time assessment if something happens to the building.

Well, there you have it. As if the condo market wasn't already challenging for a multitude of reasons, tightening lending standards being one of them, things will get even more difficult starting early next year.

One thing I always tell my buyers whenever they close on condo purchase is to get involved in the HOA. Each HOA is its own democratic government. Some are governed better than others. The common sentiment I find among problematic buildings is owner apathy. Disengaged owners, apathetic to what's happening in their building create a ripe environment for a special assessment that could have been prevented, or minimized at the least. Don't get confused, some of these apathetic owners might think their problematic buildings are challenges only for prospective buyers. Not true. This also impacts the ability for any owner to complete a mortgage refinance. Tightening lending standards apply to anyone seeking financing, not just buyers.

If I were a condo owner, I would be presenting these changes to the HOA at the next board meeting and seeing what can be done to get ahead of this. Price, HOA dues, location, layout, etc all still matter, and will forever matter when it comes to real estate and attracting buyers and/or maximizing resalability, but buyers are now growing increasingly cognizant regarding the dangers of poorly managed HOA's. A well run and prepared HOA can potentially increase the value of those units relative to similar units in poor financial health.

Other issues detering buyers; a lack of parking, no in-unit washer/dryer, and overly restrictive rules and regulations, specifically involving pets and rentals. Let's face it, Seattle treats dogs better than most human beings so not allowing any dogs, or restricting them to a weight limit, can result in lost opportunity. This is exactly what happened for a Queen Anne condo that had a full price cash buyer under contract within the first week of being re-listed earlier this year. The buyer backed out after the HOA was inflexible in amending their pet policy to accommodate their dog over 40lbs. In the 3 months since, the unit has remained unsold with not a single showing. Ouch. It may seem like an insignificant variable, but any of these deterrents can singularity be the difference between sold and stale.

Onto the stats - For March 2026, the median sale price for a Seattle condo registered $602,750. That was down 4% YoY and up just slightly MoM from $596k+. Inventory is elevated, but not by as much as it was this time last year, with 17.3% more units on the marketYoY. The months of inventory remained flat MoM at 4.54 months.

Enjoy the spring and best of luck avoiding allergies! Onward!

If the Market Feels Sluggish, It's Not You. The GSHMR for February, 2026

Welcome to March Madness!

And welcome to the latest edition of the Greater Seattle Housing Market Review. As always, to skip the good stuff and go right to the stats, you can watch them via this link here. For more infotainment, continue reading below!

As the title suggests, if the start to 2026 has felt lethargic, you're not alone. January is never robust as the market is waking up from the holiday hangover, but by February the market turns from dormant to competitive with such quickness that it catches many buyers, and some realtors, flat footed. By March, the market feels like a runaway train. A lot of change in a short amount of time.

In last month's GSHMR I reported on the "dip" that takes place every January in regard to home values. In that report I predicted that once February's data is published we'll see the market "wake up", and whatever optimism might have been gained by reading January's stats will soon be decimated once February's stats become available. We saw exactly that. See below:

Seattle: The median sale price in February registered $962,500. That is down just .26% YoY, but up massively MoM from $850,000. Inventory remains elevated with 33.8% more homes on the market YoY, but the months of inventory, which was unusually very high in January, dropped significantly to 2.68 from 3.39.

Eastside: - The median sale price registered $1,566,782. That is down 7% YoY, but up MoM from $1,435,000. Inventory remains significantly higher at 57.8% more inventory YoY and the months of inventory actually increased slightly to 3.23 from 3.17 MoM.

King County - The median sale price registered $936,000. That is up 2.3% YoY and up MoM from $850,000. Inventory remains significantly elevated at 42.4% more inventory YoY, but the months of inventory dropped to 2.71 from 2.92.

In addition to the supply/demand dynamics, there are also a number of macro, geopolitical issues going on right now that have the potential to influence the local housing market.

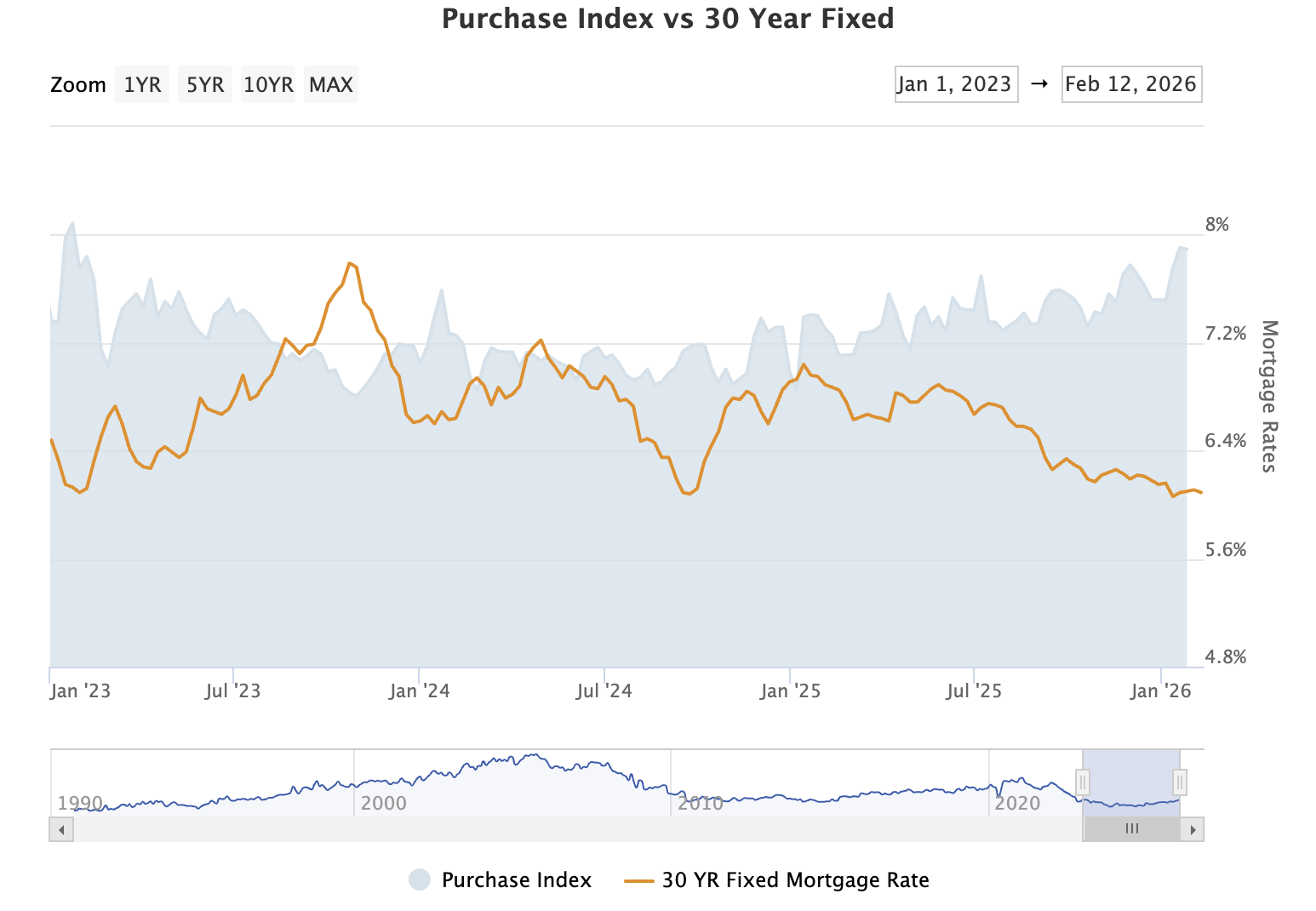

War in Iran- Obviously there are numerous consequences of a global conflict such as this one, but to be succinct I'll focus on the impact the conflict has had on mortgage rates. Historically, global conflicts are actually favorable for lower mortgage rates because of the "flight to safety" that exists when investors sell off equities/stocks and buy treasuries/bonds, the safer, less risky asset. The demand for bonds pushes mortgage rates lower. However, so far in this conflict, that has NOT been the result.

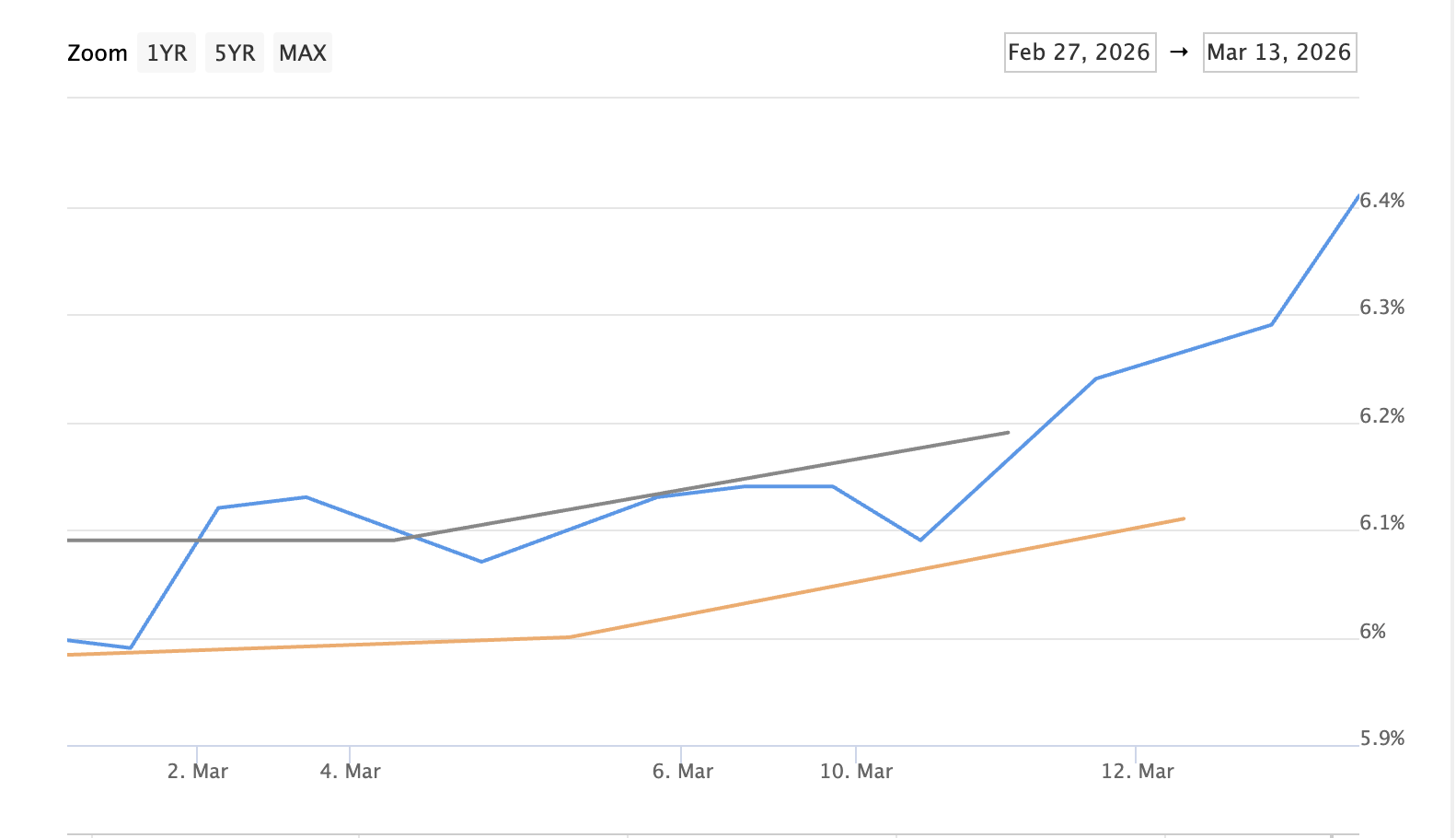

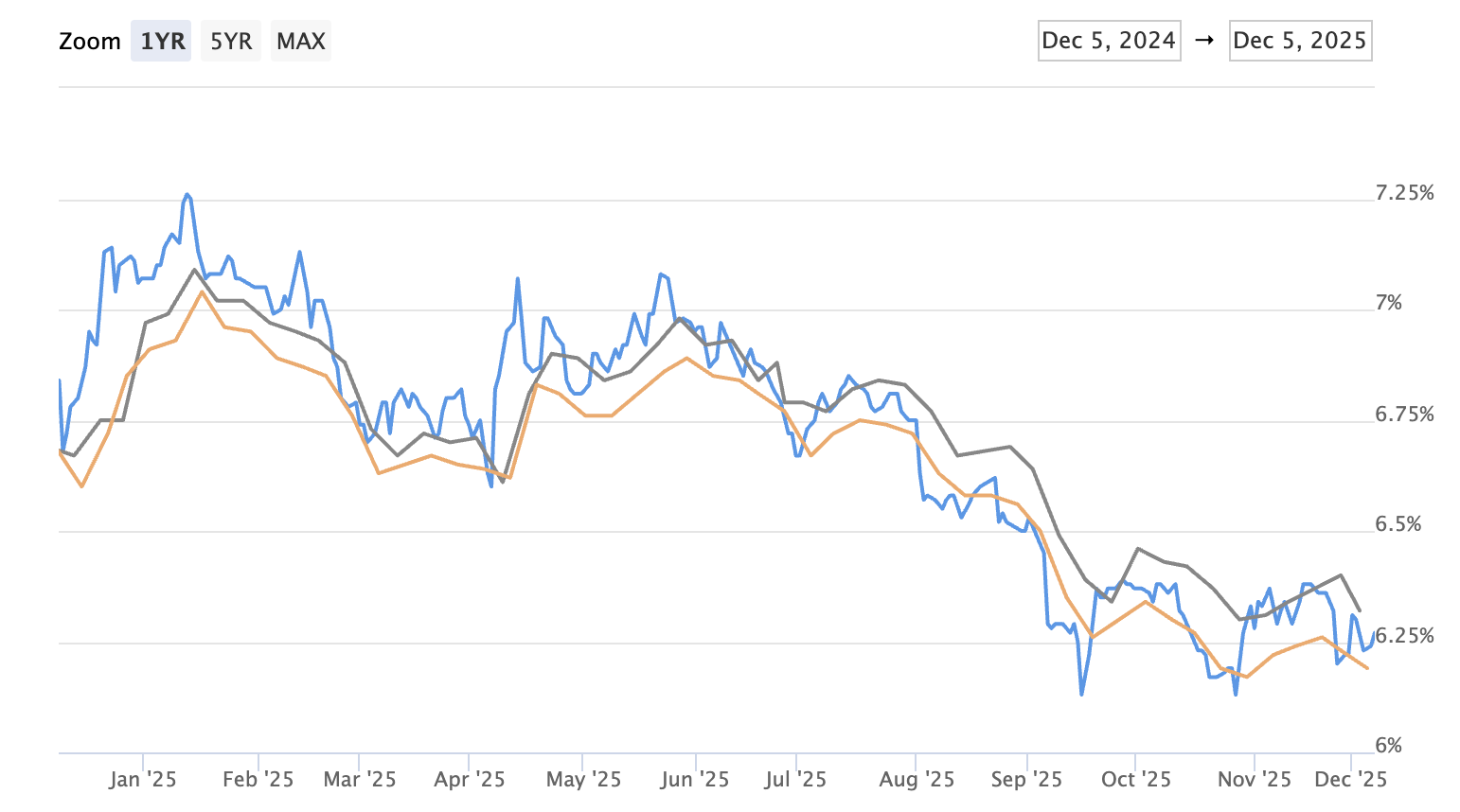

Why? Oil. Because of Iran's prominence in the global oil trade, disrupting the production and distribution of a commodity as valuable as oil is bad for inflation (just see how much the cost of oil, and gas, has risen during this active conflict). Inflation is not good for mortgage rates so despite a military conflict that is historically favorable for mortgage rates, interest rates have actually increased during this conflict. How much longer this conflict continues, and how much higher rates can potentially move, remains to be seen. See below how rates have trended from February 27th through March 13th. Rates are about .375%-.500% higher.

The labor market - This isn't specific to just 2026, but local layoffs continue to be a news headline. Of course, like any headline (or even article these days) we have to question is the reporting fact based, or based out of marketing (selling clicks)? There's some truth to both angles there, but whether based in fact or rhetoric, if someone fears their job/income isn't as stable as they prefer, that can definitely shut down their pursuit of homebuying.

"Millionaire Tax" - Washington State is getting close to an income tax applying to those making over $1,000,000/year. Even if this passes, it will be fought in courts and that will likely take time so I don't see this impacting our market any time soon, if ever. Back to the media and their need for clicks, articles like this one are detailing certain wealthy individuals, like Starbucks CEO Howard Schultz, who have already vacated to more tax friendly states. Could this impact the ultra luxury market? Perhaps, but very unlikely to cause any ripple effect from there.

However, if we see more indigenous companies like Starbucks, who just shifted corporate jobs to Tennessee, follow their lead, that can become problematic. And heck, even the Seahawks general manager said that a potential income tax could make free agent signings more difficult in attracting top talent. Don't mess with our Seahawks!!

Have an amazing March. Onward!

Maybe Things Aren't Better When Downtown? The SCMR for February, 2026

Welcome to March Madness!

Welcome to the latest and greatest edition of the Seattle Condo Market Review. I can't believe we're almost a quarter of the way through 2026! As always, to skip right to the stats, click here. For more detailed analysis, continue reading below.

To anybody not freshly new to Seattle and/or Seattle real estate, it's no surprise to read, again, about the challenging condo market within the downtown core. For context, that downtown core I define as being Belltown, downtown Seattle, Capitol Hill, First Hill, Eastlake, Westlake, and lower Queen Anne. Most condos have had their challenges over the recent years, but the downtown core has been hit particularly hard.

Many of these reasons regarding the plight of the downtown core are known to everybody, but one thing not many have discussed is the surge in apartment construction. See below:

Apartment construction has been the thorne in the side of the condo resale market. With more supply hitting the market, that's driven down rents so much to the point that sometimes it's 50% cheaper, on a monthly payment comparison, to rent the same condo than purchase. I touched on this in a past writeup referencing some specific condo units with whom I've been in discussions with the owners about selling.

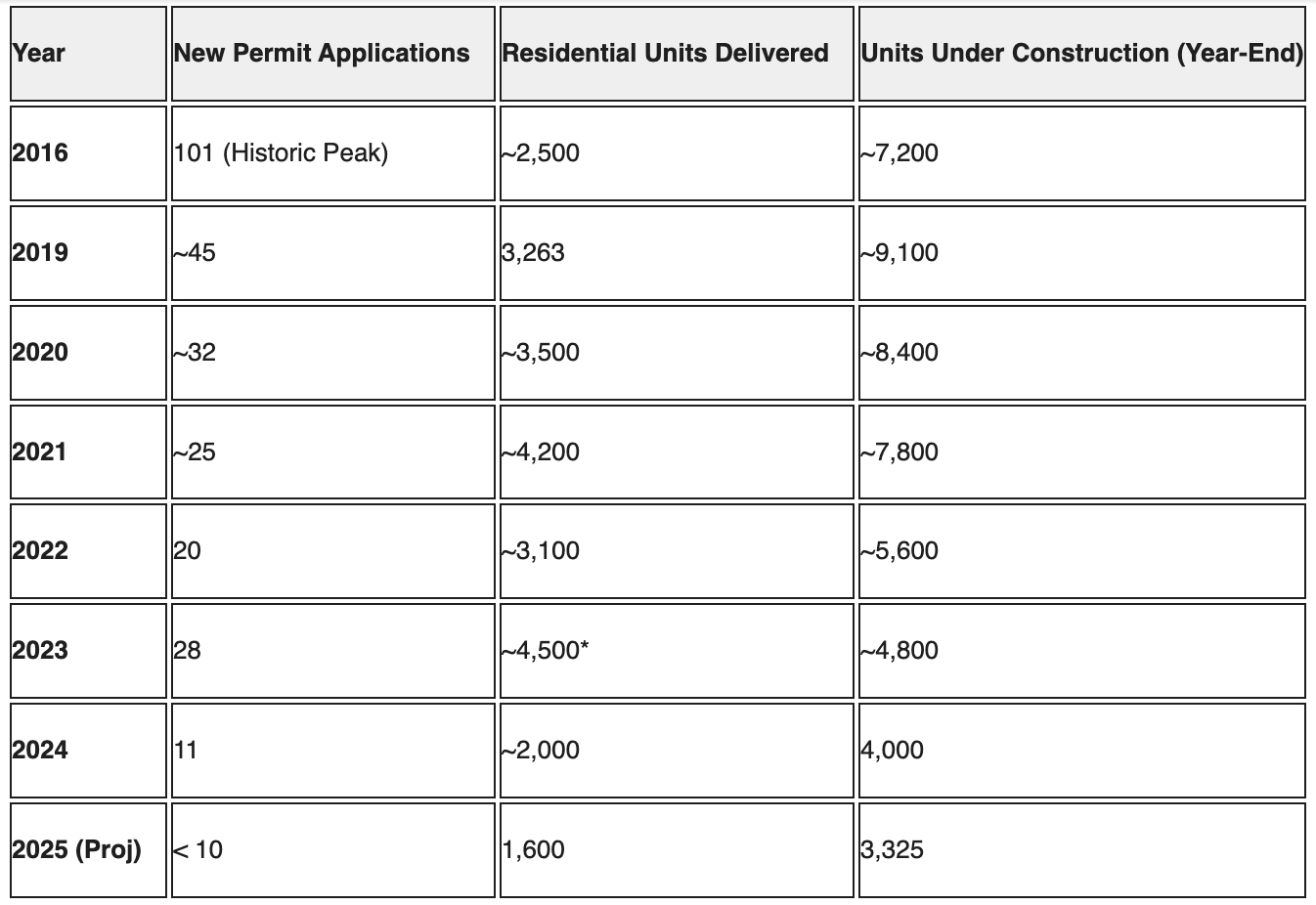

I find a few trends really interesting. First, the dropoff in multifamily permitting applications from the 2016 peak. 2024 levels were roughly 10% of 2016!

Keep in mind, it takes 2-4 years from permitting to building completion so the peak of 2016 wasn't delivered until 2019-20 and we can expect permitting starting in 2022 and beyond to deliver less and less units starting this year and continuing into next year. This makes sense considering the meteoric rise in borrowing costs (interest rates) that began in 2022. As financing gets more expensive, less units are constructed, and less delivered. This should stabilize rents, if not even provide upward pressure, possibly making condo ownership more desirable than in recent years. This can be especially true if the downtown population continues to increase beyond 2025 all time records.

To be clear, I'm not prophesying that this is the magic bullet to cure the condo market. Just as I said about the return to work orders, a possible FHA/VA approval savior, and now the lack of apartment supply. There are still exterior headwinds in affordability that persist, but this is true for every property type in every market.

Onto the stats:

The February 2026 median sale price registered $596,275. That is down 4.6% YoY, but up MoM from $557,000. Inventory remains elevated at 19.6% more on the market YoY, but the months of inventory dropped to 4.64 months from 5.39 the month before.

Enjoy St. Patrick's Day, March Madness, and the Mariners opening up their 2026 season. Onward!

A Buyer's Market to Start 2026. The GSMCR for January, 2026

I hope you've been properly celebrating your 2026 Super Bowl champion Seattle Seahawks!!

Back to business and welcome to the latest Seattle Condo Market Review. As always, to jump right to the stats, you can watch that video by clicking here. For more detailed information, continue reading below!

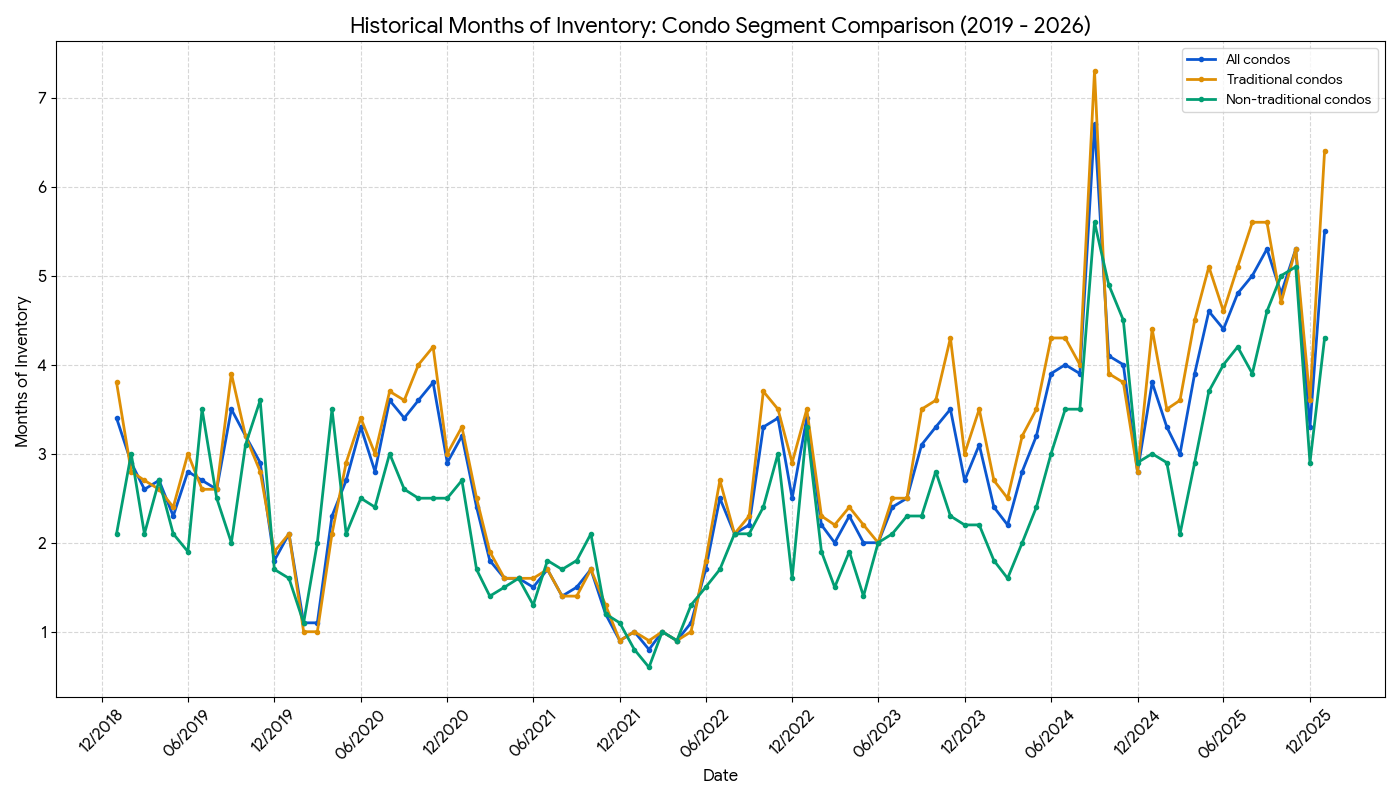

I apologize for the above chart not being the most visually easy to read, but regardless, what I want to highlight is this: We're entering the year already in a buyer's market for Seattle condos.

it's true. The blue line represents all condo types, the orange line represents traditional condos (one story), and the green line represents non-traditional condos. The latter are going to include the new construction condos we refer to as condo-ized homes or DADU's.

A neutral housing market is roughly 3-4 months worth of inventory. Late Q4 and early Q1, historically, represent the lowest levels of months of inventory because overall inventory is much less compared to the summer and fall months. For the entire condo market to start the year at over 5 months of inventory is definitely NOT what I was wanting to see if 2026 was going to offer relief for the condo market. Of course, we have a LONG way to go so I'm not putting a fork in the condo market just yet. That being said, we're working off quite the deficit.

At least nationally, mortgage applications from borrowers looking to purchase are at their highest levels in 3 years. It's a small victory. Not one that will save the local condo market, at least not any time soon, but it's a start. I still feel the best friend for the Seattle condo market moving forward will be the decline of new apartment construction though I don't expect that impact to start making a difference until next year at the earliest. Perhaps more on that later in a future edition.

Onto the stats :

The median sale price for a Seattle condo in January registered at $557,000. That is down 19.3% YoY and up, just barely, MoM from $555,000. Inventory remains elevated with 21.6% more units on the market YoY. The months of inventory statistic increased significantly YoY to 5.39 months from 3.02.

I hope you all properly celebrated the Seahawks Super Bowl victory! Below is a picture a colleague of mine found. Sadly, despite this person having a striking resemblance to me, I can confirm this is not me. But I can assure you we shared the same spirit that day. Go Hawks!

Onward!

Buy the Dip? The GSHMR for January, 2026

Welcome to the latest edition of the Greater Seattle Housing Market Review. As always, to skip right to the stats, click here. For more information, continue reading below!

As the title suggests, January produced some pretty sluggish numbers for a number of different metrics. And as I've reported on in the past, this is the "dip" before the market begins to take off. See my report here I wrote just a few months ago on this topic.

However, while January every year is a step back before taking multiple steps forward, 2026 started off with more of a setback than what we're used to seeing.

Starting with the median sale prices, Seattle saw the lowest median sale price ($850,000) since December of 2023. The Eastside ($1,435,000) wasn't this low since November of 2023 and King County as a whole ($850,000) wasn't this low since January of 2024.

While the absorption rate for Seattle was the highest it has been since July, it was still the lowest January reading since I've been collecting this data going back to 2019. Additionally, it wasn't even close with buyers absorbing inventory at roughly 25% less than January of 2025.

What surprised me the most was the months of inventory. Typically, January is one of the lowest points in the year for this metric as inventory is always slow to pick back up after a dormant end to Q4. Surprisingly, this number increased for each area month over month and was up quite significantly year over year.

The graph below I used in a report about 3 months ago to show how, every year, January represents the low point for property values before they take off in the next 4-5 months. (This was for King County)

Given what we've seen the last 10 years (and beyond, I chose not to include any more history for the purposes of keeping this as succinct as possible) we're just getting out of that "dip" before values historically begin to take off.

Does this mean buyers have missed the boat? No, not at all. Some of the reason as to why values in January are depressed relative to the rest of the year is because much of what's selling in January was listed in October, September, August, etc and thus sat on the market for a few months, had one or more price reductions, and overall sold under the asking price.

What I'm seeing anecdotally right now suggests the opposite as multiple offers are back. I've even seen a few cases where properties that had been sitting on the market dormant for 70+ days suddenly received multiple offers. Perhaps some of this can be attributed to the graph below:

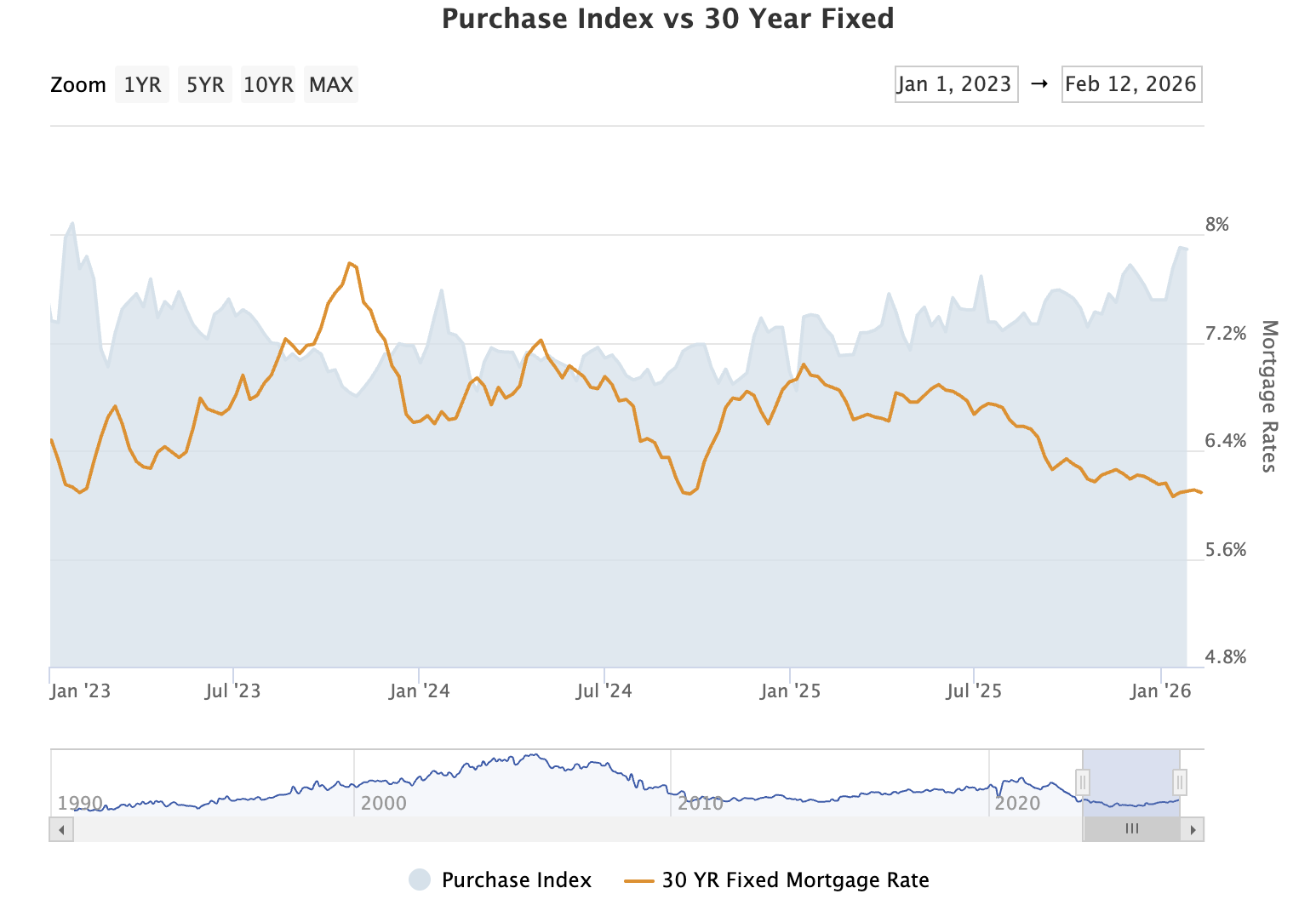

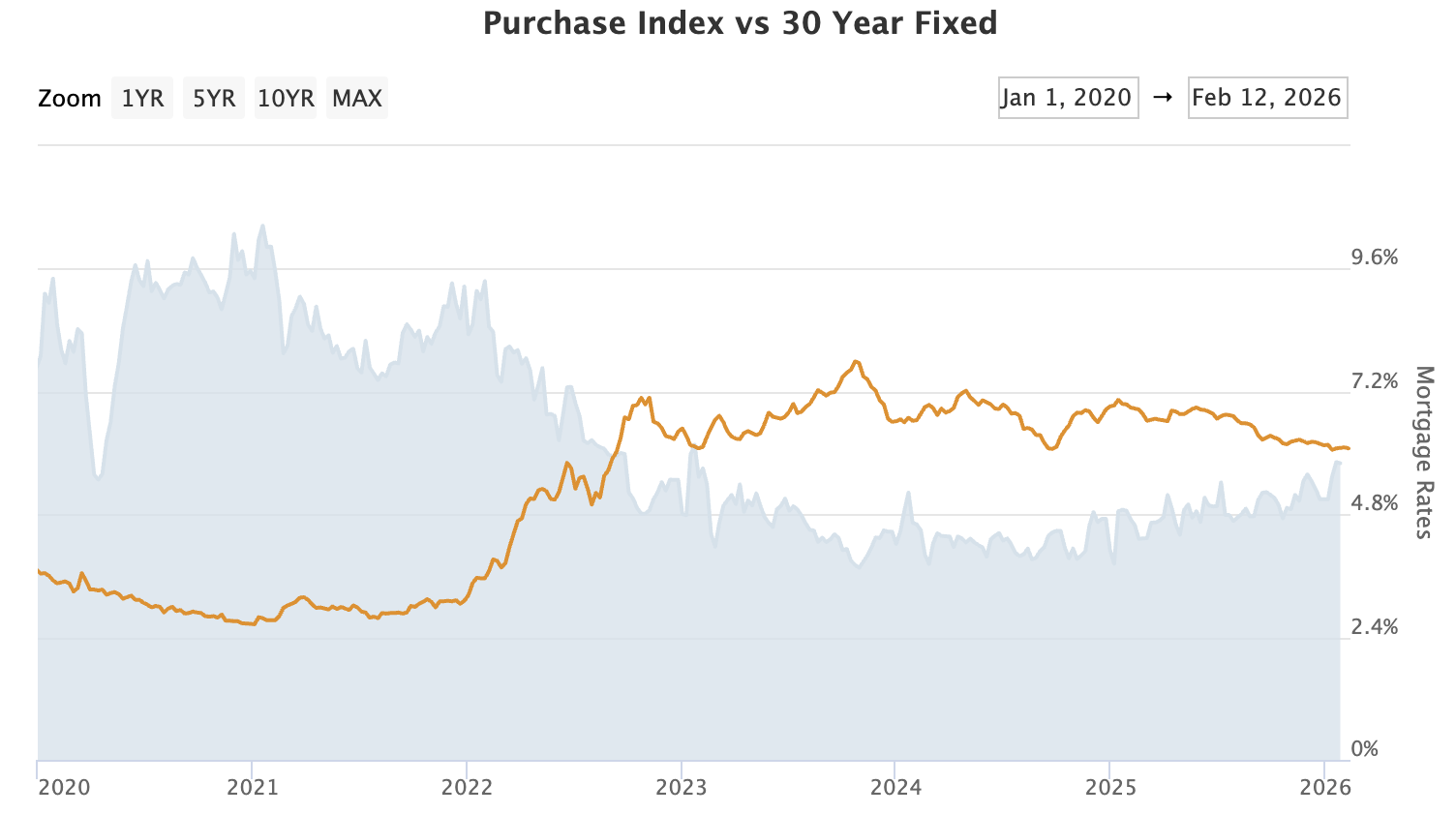

Above, in the dark shaded data, is the purchase application index that tracks national purchase applications for mortgage applicants. This January we reached levels we have not seen since January of 2023.

Before we throw any parades, let's keep in mind that these figures are still roughly half of what application rates looked like during the post Covid bubble (see above). Still, there's hope that this might signify we've passed the bottom and are on our way out of the housing recession we've been in for almost 4 years. More buyers applying for mortgages is a pretty obvious precursor to more homes being purchased, right? Time will tell.

Onto the stats: A little anticlimactic since I already discussed these, but nevertheless, here we go!

Seattle - January 2026 median sale price of $850,000. that is down .87% YoY and down from $914,000 MoM. Inventory was up 29.9% YoY and the months of inventory statistic increased dramatically MoM to 3.39 from 2 months.

Eastside - Median sale price of $1,435,000. That is down 16% YoY and down MoM from $1,500,000. Inventory remains elevated at 49.34% more homes on the market YoY and the months of inventory rose to 3.17 from 1.58 in December.

King County - Median sale price of $850,000. That is down .58% YoY and down MoM from $900,000. Inventory is up YoY b 31.13% and the months of inventory rose to 2.92 from 1.68.

I hope you all properly celebrated the Seahawks Super Bowl victory! Below is a picture a colleague of mine found. Sadly, despite this person having a striking resemblance to me, I can confirm this is not me. But I can assure you we shared the same spirit that day. Go Hawks!

Onward!

Stale rents = paused buyers; The Seattle Condo Market Review for December 2025

Happy New Year!

And just like that we're into 2026 and 1/4th of the way through the 21st century. Wild!

Welcome to the latest edition of the Seattle Condo Market Review. As always, to jump forward straight to the stats, you can do so by clicking here. To get deeper context into everything Seattle condo related, continue below!

For those of you who have been consistently reading these reports over the years, you're probably well aware of the challenges I've had in trying to report on something new month after month in a market that's been so, well, challenging. I'm going to come right out and say it, I don't think 2026 is going to be any different. I hope I'm wrong.

What does it take to get a home sold? It takes a listing (supply) and demand (a buyer). I know, duh, a real brain buster of a question. We know that inventory/supply has not been kind to the condo market for the past year and beyond, but we also know demand has been oppressed too thanks to affordability challenges with increasing mortgage rates, insurance costs, HOA dues, etc. However, I want to explore a less talked about challenge to getting condos sold. Flat rents and a significant disparity in the mortgage to rent ratio.

Historically, rising rents are the best incentive for buyers to kickstart their homeownership journey. Not because homeownership is less expensive than renting, but if the figures are close enough, it makes sense hedging one's housing cost and investing into real estate vs paying someone else's mortgage month after month. The problem the condo market is seeing right now is totally different. Renters are staying put because their rents aren't increasing AND the value of condo ownership hasn't produced the return on investment it did years ago.

I'm going to share some real life examples for condo owners who have reached out to me about selling, some who have had their units rented out recently, so I can directly convey these challenges in real time.

An owner of a Belltown studio was recently receiving $1,700/month in rent. It was a studio unit and I estimated it could sell for $260,000, or thereabouts. If a buyer were to purchase this unit at $260,000 and put 20% down while financing the home at 6%, the buyer's total monthly payment, including HOA's, would come out to $2034. As a consumer, would you rather pay $1700 or $2,034 AFTER dropping $50,000+ into a down payment?

Another Belltown condo owner, this time of a 1 bedroom unit is currently receiving $2200/month in rent. Their total mortgage + HOA payment was in excess of $2,600/month. So they were already losing roughly $400/month in negative cash flow. Yikes. I estimated that $350,000 would be a sensible price for this unit so with a 20% down payment, financing at 6%, all the same factors from above, that would equate to a monthly mortgage payment of $2,796/month. Roughly a $600/month difference, or 27%+ more to buy vs rent.

Moving outside of Belltown, a Queen Anne condo owner contacted me who currently has their unit leased for $3,000/month. Not bad at all for a 1 bedroom unit. The problem here is that this building has extremely high HOA dues of $1,493/month. Buying that unit today at $575,000 (which would be a little less than what the unit was purchased for in 2019) would equate to a total monthly mortgage payment (plus HOA's) of $4,851/month. 61.7% more than what the unit is currently rented for. Wow.

Don't get me wrong, the monthly payment has historically almost always been higher on a mortgage vs rent comparison so I'm not suggesting it only makes sense to buy when the numbers are close or when it's more expensive to rent. The problem I'm highlighting is when buyer's aren't seeing the value of the asset they're investing in AND they can rent the exact same unit for a fraction of a monthly payment vs owning, what's compelling them to pursue condo ownership? Especially with inflation staying elevated everywhere else, the ability to keep your housing costs minimized is likely paramount to many Seattleites.

Onto the stats:

The median sales price for a Seattle condo ended 2025 at $550,000. That is up .9% YoY and down MoM from $573,500. Inventory was up 13.8% YoY but the months of inventory stat declined significantly to 3.02 from 5.41 months in November. We also notched the highest absorption rate metric since March (likely due to all those units being pulled from the market in December).

Lastly, I'm hosting a FREE Home Buying seminar on February 7, 2026 at Ivar's Salmon House in North Lake Union. It's from 10-11:30 and if you'd like to come, you can RSVP here. If you know of anybody else who might be interested, feel free to forward to them.

I look forward to connecting more in 2026. Onward!

Fun With Demographics; The Greater Seattle Housing Market Review for 12/2025

Happy New Year!

And just like that, we are now 25% through the 21st century. Holy cow.

Welcome to the latest edition of the Greater Seattle Housing Market Review. As always, to skip the reading and jump right into the stats, you can do so by clicking here. For the rest of you, continue below!

As a Seattle Times subscriber, I've found the FYI Guy (Gene Balk) to consistently have some interesting articles. He's not the real estate beat writer for The Times, in fact his articles aren't ever about real estate, but it's not a stretch to find parallels between a few recent articles and the current, and future, outlook for our local housing market.

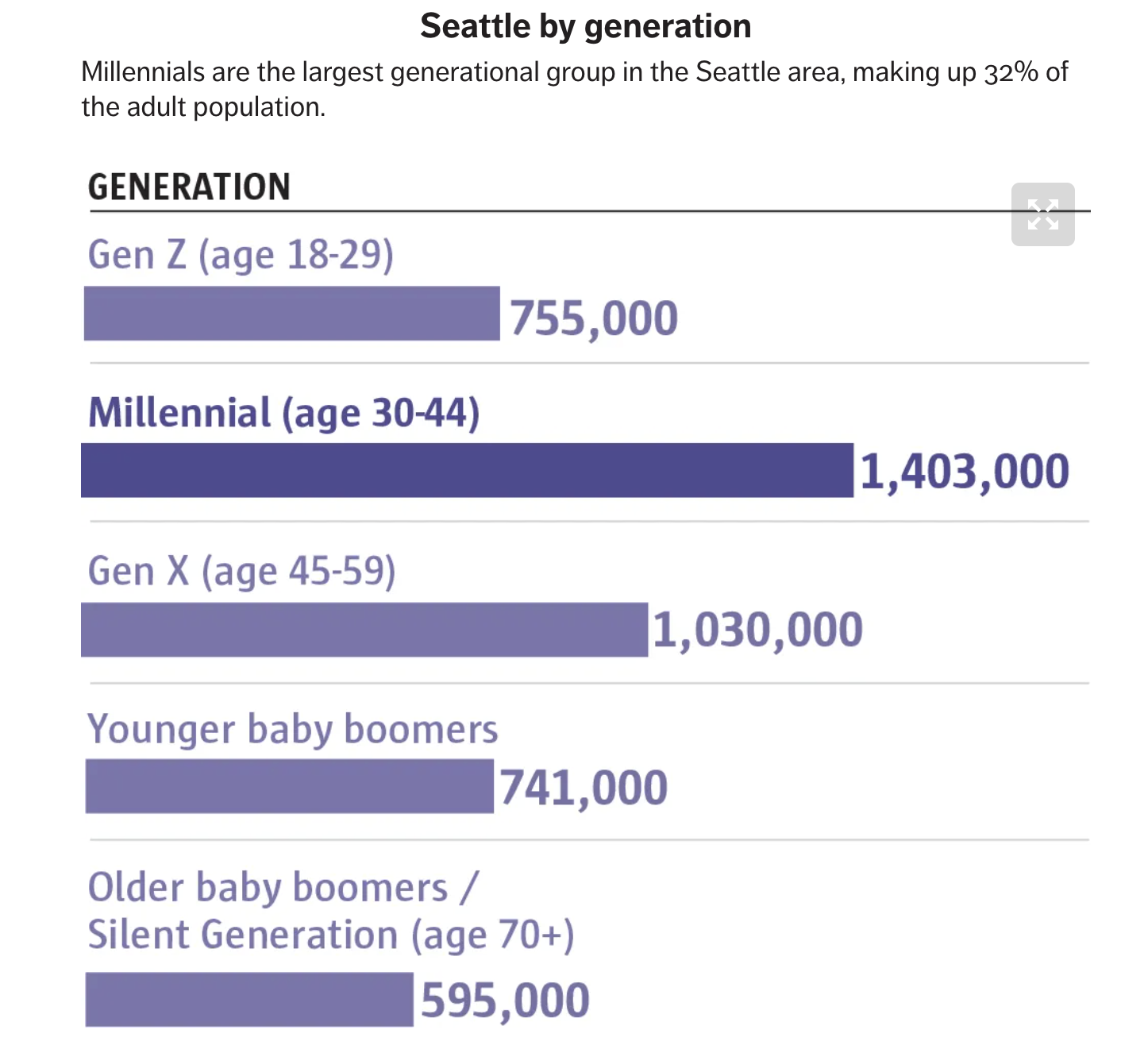

For starters, this story, published in mid December, identifies millennials as being the most populous generation in the Seattle metro area, accounting for over 1.4 million residents. This is largely due to the increase in millennials moving to Seattle during the 2010's while the local tech industry was on a hiring craze.

But what do we also know about millennials? We know that the median age of a first time home buyer has been increasing over the last number of years, finishing 2025 at 40 years old. There are many articles on this, but I'll link the article from NAR here.

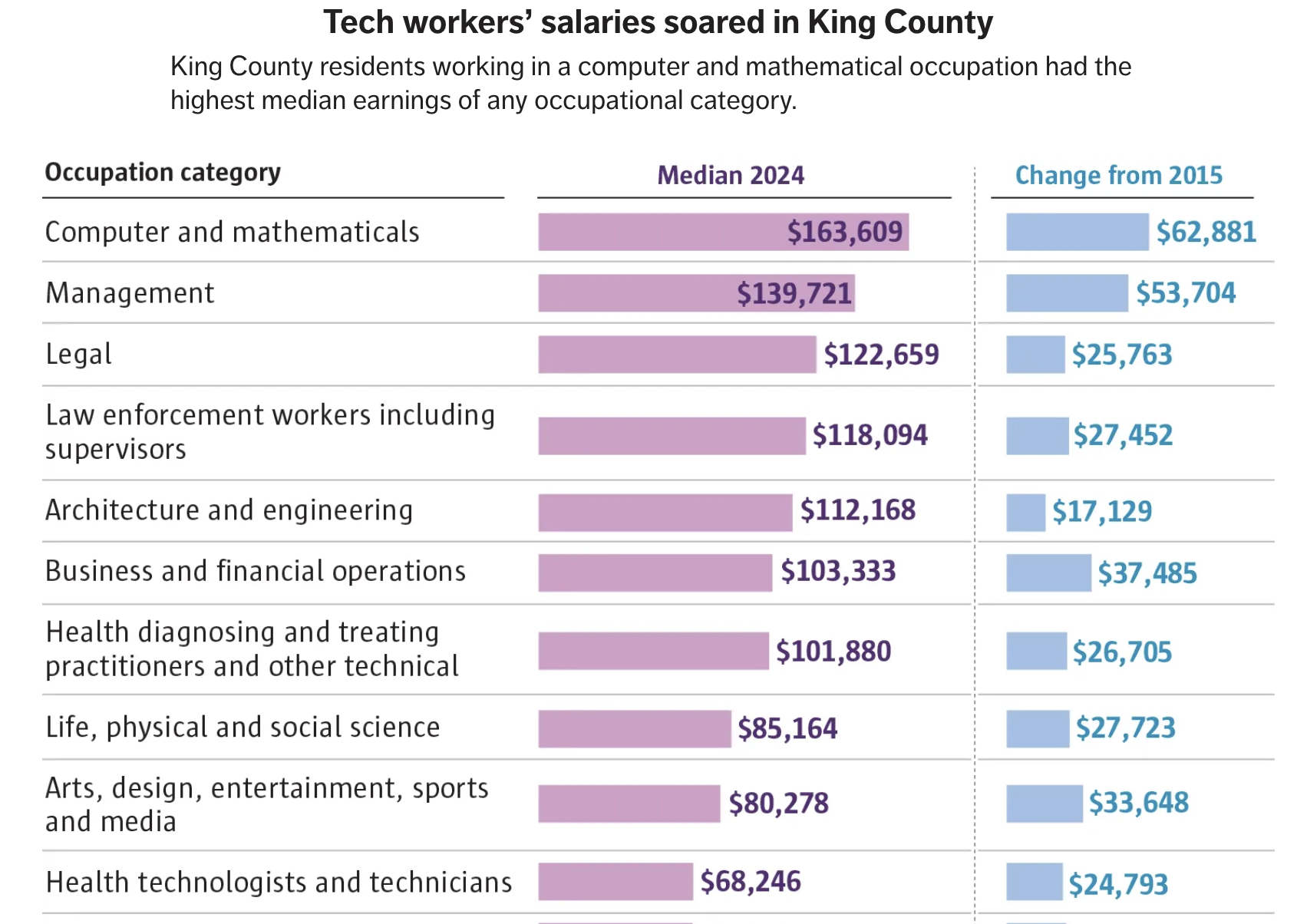

Circling back to tech, on December 9th the FYI Guy published this article, documenting the soaring pay within the tech industry over the past decade. See below the chart showing the gain in median incomes within different industries from 2015-2025.

Quick note; I'm always excited when they source data based around the median rather than the average since, especially with tech salaries, using the average could really swing the data dramatically. As a data nerd, I really like that and wanted to give a tip of the cap.

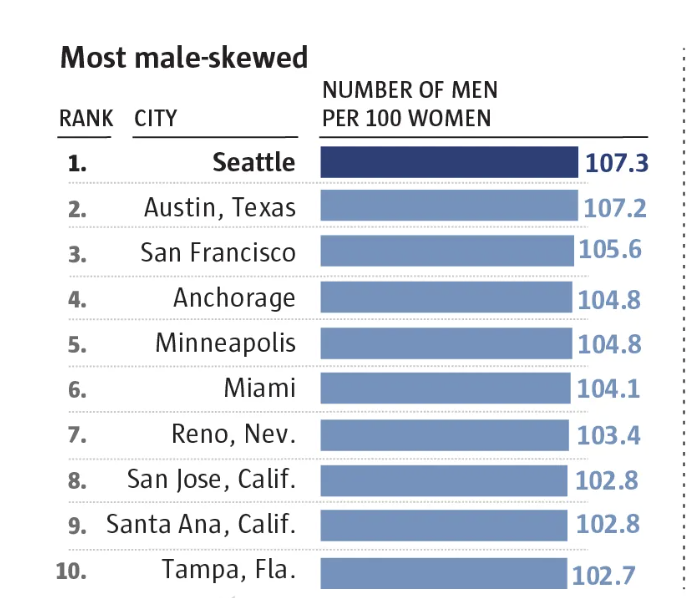

Another big take away I had in this article was the increasing pay gap within the tech industry. It's no secret just how male dominated the tech industry has, and continues to be, but it was surprising to see the gap between men and women actually increase from 2015-24. From the article, "in 2015 women in tech made 87.9% of what men earned. In 2024, that figure fell to 78.7%".

Finally, this article published back in June, illustrates the gender divide and how Seattle was ranked the most male dominated big city within the country! For every 100 women in Seattle there were over 107 men. Personally, I don't feel that's too big a gap, but was still surprised that it was enough to rank us #1 in the category. Fellas, if you're looking to find the big city where the number of women are most outweighing men, check out Baltimore that had roughly 100 women for every 82 men.

So what does this have to do with real estate? Well, perhaps nothing. Or maybe it's telling us something? If we combine each of these articles, it more or less fits into the narrative that your average Seattle area home buyer is a millennial male working in the tech industry. Below are AI generated images of these individuals. Maybe you've run into them at an open house?

Obviously, this is somewhat of an overgeneralization (and hopefully a comical one), but the basics ring true. Young-ish people with money are buying homes. Does that mean everybody who doesn't fit into this narrow demographic is SOL? Of course not. Personally, very few of my clients fit into this mold and everybody's situation is different.

What I do know is regardless of your financial situation, if you're looking to get started in your home buying journey for 2026, buckle up for a competitive start to the year. Every year we see competition peak in Q1 and early Q2 setting up a huge chunk of the overall appreciation for the entire year. What could add to the intensity this year is the declining mortgage interest rate.

Interest rates today are roughly a full point lower than they were at this time last year. Lower borrowing costs means stronger buyer purchasing power which push home prices higher. You heard it here again. Buckle up!

Onto the stats:

Seattle: The median sale price in December 2025 registered $914,000. That was up 1.7% YoY and down from $973,500 in November. Inventory was up 28.6% YoY while the months of inventory dropped to 2 months from 2.65.

Eastside: The median sale price registered $1,500,000. That is down 2.9% YoY, but up MoM from $1,430,000. Inventory remained relatively ballooned at 64.7% more homes on the market YoY, but the months of inventory significantly decreased to 1.58. months from 2.41.

King County: The median sale price registered $899,950. That is up 2.9% YoY, but down MoM from $915,000. Inventory was up 34.6% YoY while the months of inventory statistic dropped from 2.31 to 1.68 months.

Those months of inventory stats are a foreshadowing into the competitive Q1 and early Q2 market. Dust off your boxing gloves, for certain properties, it's going to a bloodbath out there. Don't say I didn't warn you

And finally, I'm hosting the first Home Buying seminar of 2026 including a FREE brunch at Ivar's Salmon House in North Lake Union. The event is Saturday, February 7th, from 10-11:30. If you'd like to come, please use this link to RSVP. If you know of anybody else who'd benefit from this info, please send their way!

Onward!

The Calm Before the Storm; The Greater Seattle Housing Market Review for November 2025

We've almost made it past 2025!

Welcome to the latest edition of the Greater Seattle Housing Market Review. You might have noticed I'm slightly changing the wording of the title to reflect the previous month, since that's the data I'm referencing, as opposed to the month in which I create the report. This is also designed to provide more consistency to the blog feature on my website (recently revamped, check it out). As always, to skip the good stuff and go right to the stats, click here.

I create this writeup every year at this time, probably even plagiarizing the title year after year. At this moment, the market is dormant. New listings have been virtually non-existent since the beginning of November, leaving the few buyers out there with not much to look at or choose from. The result is that the market limps to the finish line at the end of the year like a wounded runner crossing the finish line at the conclusion of a grueling marathon. However, thanks to historical trends we can set our watch to, we know we're currently experiencing the calm before the Q1 storm. And when that storm hits, watch out.

There are a number of factors that can potentially contribute to a more robust housing market in early 2026. Many of which I've discussed in the past (and will do so again), starting with one that I don't think gets much attention; increasing conforming loan limits.

Increasing Conforming Loan Limits: Every year, Fannie Mae and Freddie Mac adjust their conventional loan limits based on changes in local housing markets (these increase every year). They recently announced that in our area (King, Snohomish, and Pierce counties) the maximum 2026 conventional loan limit will be $1,063,750. That's the loan amount, not the price. Given that buyers can purchase a home utilizing conventional financing with as little as a 5% down payment, that means a buyer could purchase a home priced at $1,119,000, put 5% down, and qualify for conventional financing. Of course, they'd still have to financially qualify for this monthly housing payment, which wouldn't be cheap, but it's all possible. As conventional loan limits increase, that means buyers can qualify for conventional financing at higher purchase prices, which could push prices higher.

Steady, if not lower, mortgage rates:

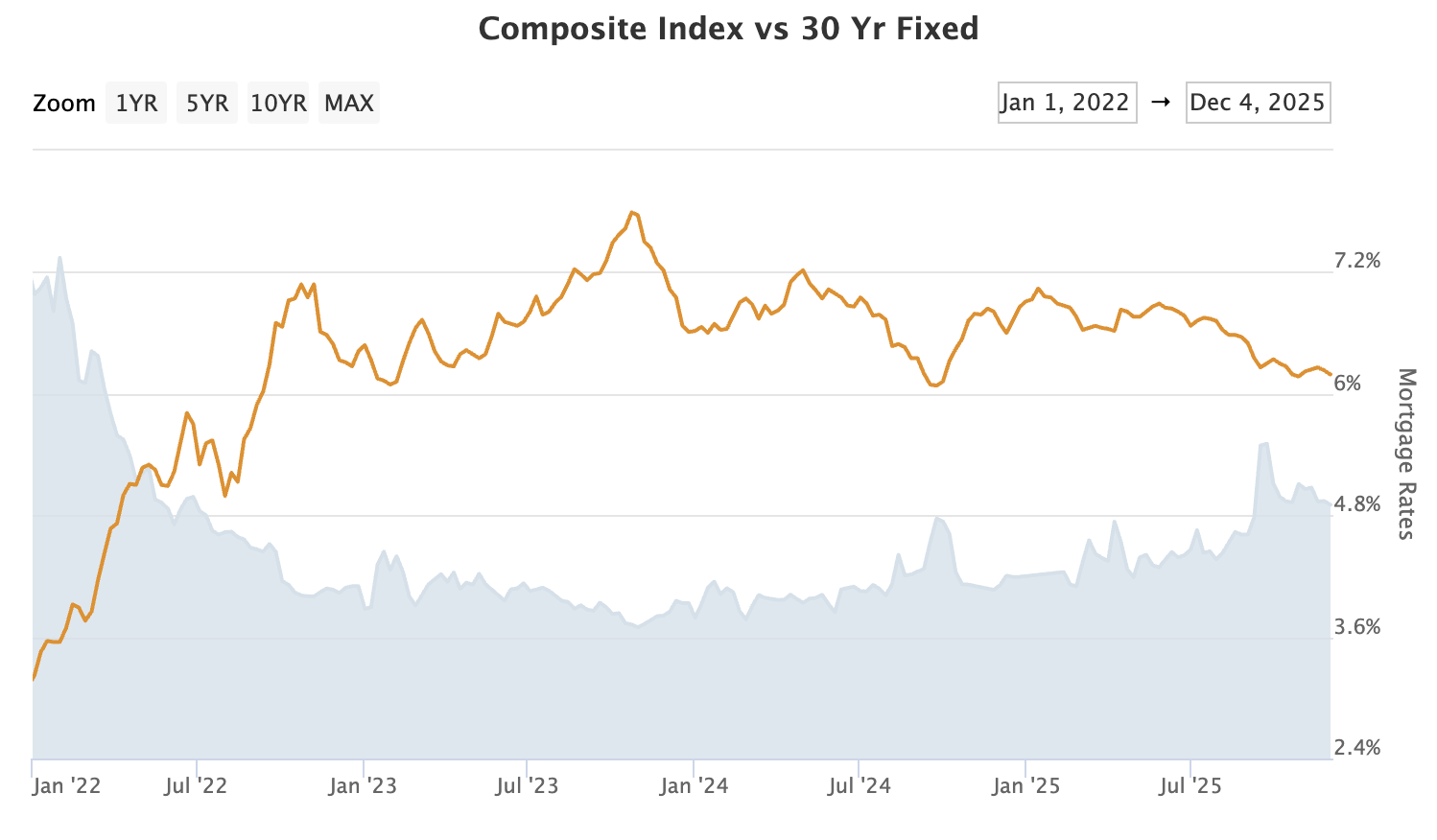

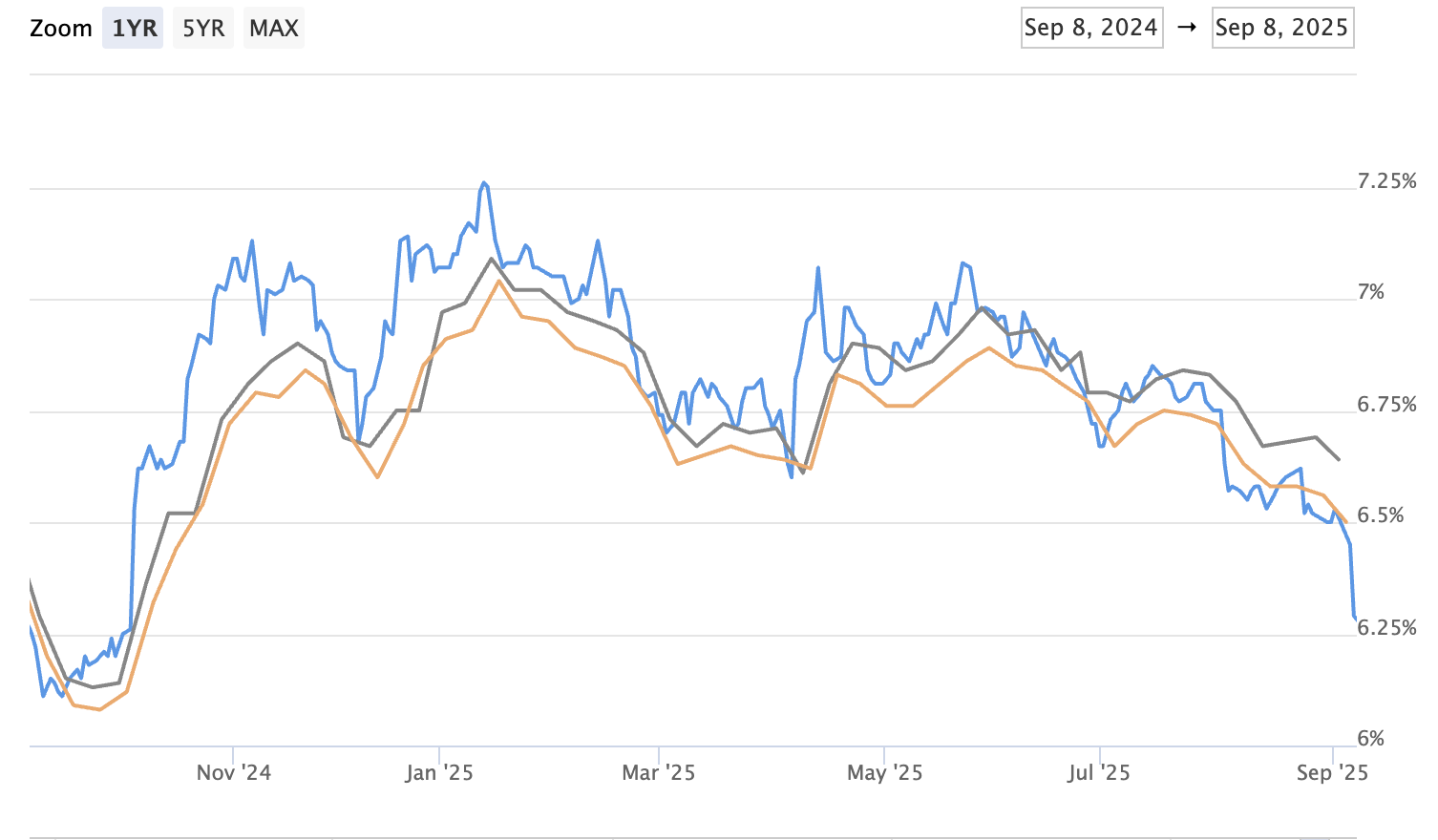

Look at how the 30 year mortgage interest rate has tread lower over the last year. It's not anything worth throwing a parade over, but they've come down .5-.75% during this time, which certainly helps from an affordability standpoint. Redfin recently published their 2026 housing outlook and they project interest rates to remain in the range in which we're currently sitting (low 6's). Personally, I feel that as long as mortgage rates are stable and not volatile where there are wild swings up or down, that stability creates consumer confidence, which brings more buyers into the market.

If rates not only stay where they're at, but actually trend lower, that could bring even more buyers into the market. A number to watch on this will be the unemployment rate. At the time I'm creating this report, the unemployment rate is 4.4%. The Federal Reserve has clearly shown their preference for labor data or inflation data in justifying interest rate cuts, but if the cracks within the labor market widen and turn into bigger issues, the Fed will feel increasing pressure to reduce their rate, which will send the 10 year treasury note below the current technical levels keeping mortgage rates in the low 6's. If this happens we could see rates in the high 5%'s (remember, the 10 year T-bill is what sets the 30 year mortgage, not the Fed funds rate). Of course, as discussed in previous reports, adjustable rate mortgages are already sub 6% so taking out an adjustable mortgage that's fixed for 7 or 10 years is more attractive than it's been in over a decade given the spread relative to the 30 year fixed. Lower rates could bring more buyers into the market, which can push prices higher.

Seasonality:

You're probably all tired of hearing me say this over and over again, but we have a very predictable housing market when it comes to seasonality. Thanks to decades worth of data, we know the first 4-5 months of every year are the most seller friendly. That is because of two things; low inventory and strong buyer demand.

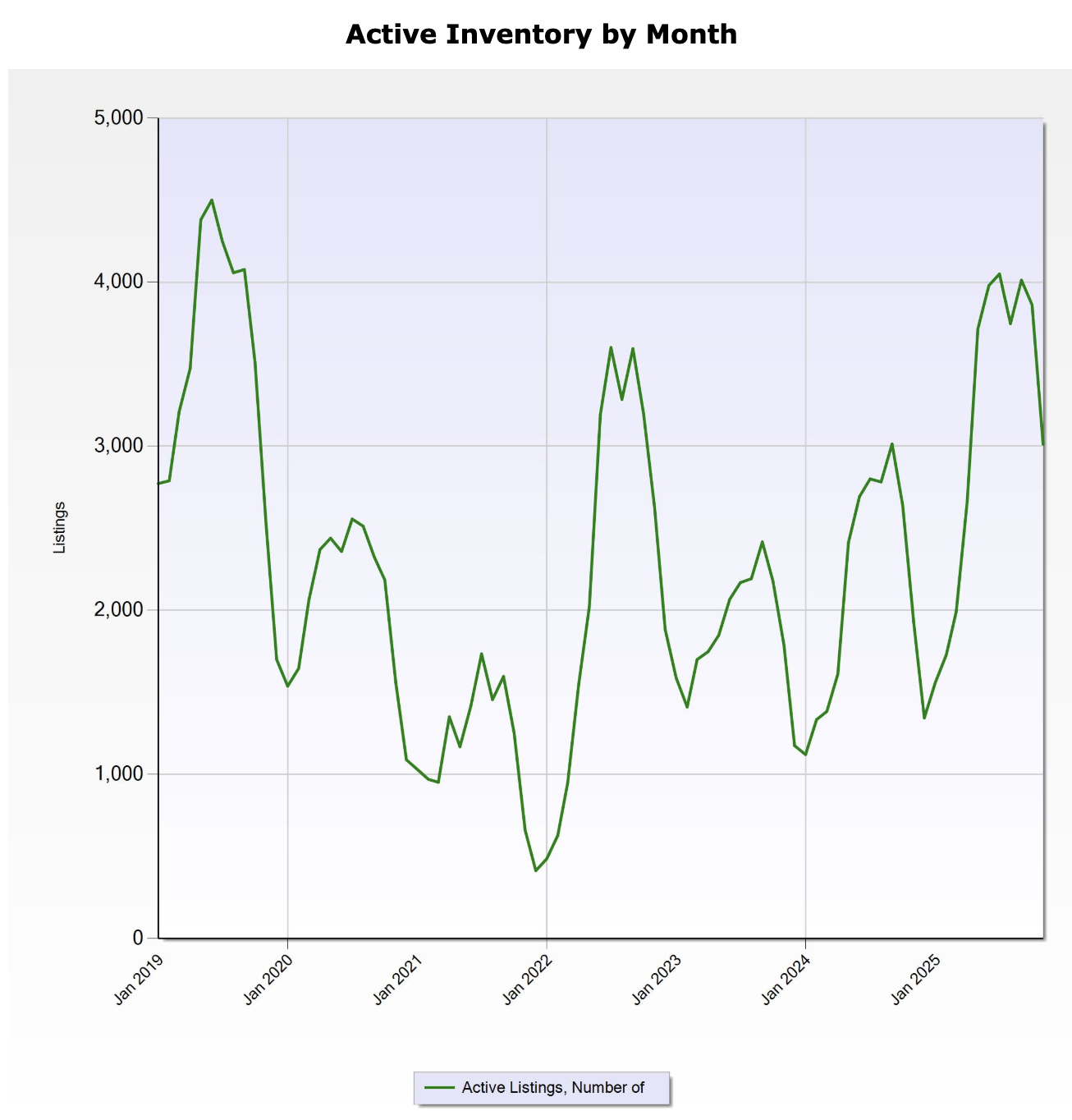

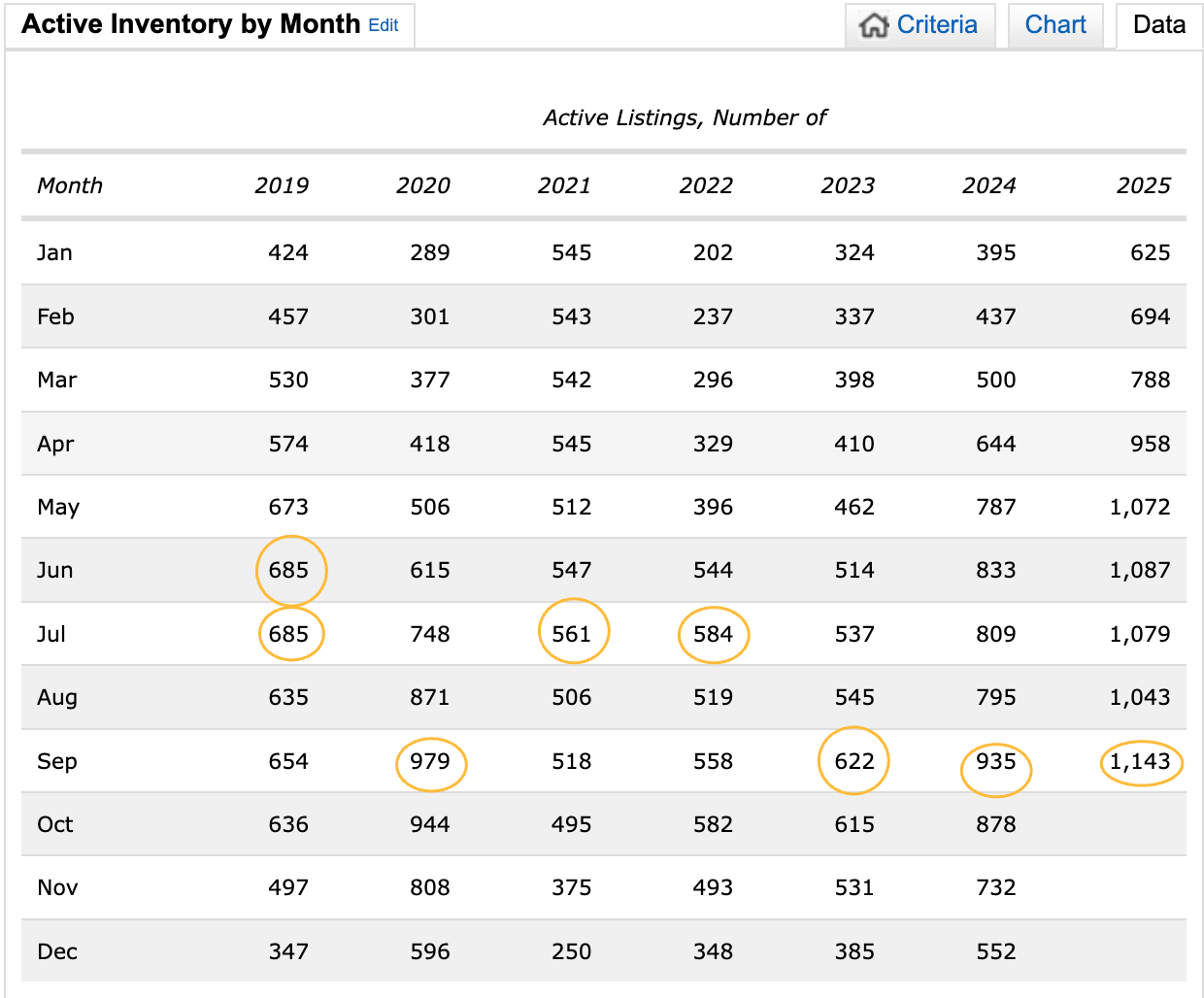

(King and Snohomish County active inventory chars above, respectively)

Inventory is always at the lowest point for the year every January. From there it builds throughout the year, peaking anywhere between July and October, depending on the year.

(Above) It's not the most obvious visual, but absorption is at its peak in the March-May timeframe of the year. Just look how insane the absorption was prior to the rapid interest rate increase during the summer of 2022.

Many of you are probably rolling your eyes because you've read or heard me preaching about this for years, maybe even experiencing it yourselves, but I'll throw one final curveball not yet discussed: new purchase mortgage application data.

Mortgage purchase applications are at their highest level since April of 2022.

While every Q1 and early Q2 are defined by low inventory, strong buyer activity, and sometimes fiercely competitive multiple offer situations, it's not crazy to suggest we might be in for a more intense, more seller friendly housing market than what we've seen in recent years. Buckle up!

Onto the stats:

Seattle: The November 2025 median sale price was $973,500. That is essentially flat YoY (up .57%) and down MoM from $1,050,000. Inventory was up 32.4% YoY and the months of inventory statistic actually increased MoM to 2.65 from 2.30. Seattle also set a new low (previous low was October 2025) for the lowest absorption rate since I've been tracking (2019).

Eastside: The median sale price was $1,430,000. That is down 7% YoY and down MoM from $1,550,000. In fact, November's reading was the lowest median sale price on the eastside since November 2023. Inventory is up 72.6% YoY and the months of inventory stat was flat at 2.41 months.

King County: The median sale price was $915,000, down 1.1% YoY, and down MoM from $997,000. Inventory is up 35% YoY and the months of inventory remained flat at 2.31 months.

Have a wonderful holiday season and enjoy time with your friends and family. We'll reconnect in 2026!

Wrapping up a Lackluster Year. The Seattle Condo Market Review, November 2025

We're almost through 2025! I hope your year has been fantastic and you're poised for an even better 2026!

Welcome to the latest edition of the Seattle Condo Market Review. You might have noticed I'm slightly changing the wording of the title to reflect the previous month, since that's the data I'm referencing, as opposed to the month in which I create the report. This is also designed to provide more consistency to the blog feature on my website (recently revamped, check it out). As always, to skip the good stuff and go right to the stats, click here.

As my reports have made painfully clear (I hope) over the past few years, the Seattle condo market has been challenging, to say the least. Thankfully, with help from myself and a few other real estate colleagues, the Seattle Times has done a solid job on reporting about this. You can read their most recent article (featuring me) here. If you can't get past the paywall, there's a similar article (though not featuring moi), here.

Above, I'm tracking the median Seattle condo (not including the newer construction DADU/condo-ized units) since January 2022. As you can see, the chart is very flat. I chose to focus on 2022 since it was in the middle of that year when we really saw interest rates start their rapid ascent.

However, even when I date this back to 2018, the data is still very much the same. Not great.

Redfin posted their 2026 housing market outlook. You can access that here, but it's not filled with any hot takes. Keep in mind, this is their outlook for the entire nation. In next month's report, I'll include my thoughts for the Seattle market in 2026.

Onto the stats: The November 2025 median sale price for Seattle condos registered $573,500. That is down just $1,450 YoY and down just $4,000 MoM. Inventory is up 20.8% YoY and the months of inventory stat increased to 5.41 months from 5.2. Absorption remains very poor.

That's a wrap on 2025! I hope you all have a fantastic Holiday season ahead. I'm looking forward to connecting with you in 2026. Onward!

Challenges with HOA's when buying/selling. The Seattle Condo Market Update, November 2025

Welcome to the latest and greatest edition of the Seattle Condo Market Update. As always, to jump straight into the stats, you can do so by clicking here. For those looking for more (and better) info, continue below!

As I've mentioned in previous reports, I struggle to find material for this report each month as the condo market has been so bland all year long. In this report, I thought I'd mix it up a little bit and discuss a variety of topics crucial to selling a condo in today's market. Bear with me.

Financial strength of HOA: Especially in markets like we're in right now, the financial health of an HOA is crucial in determining the marketability of a unit. What we're seeing right now is that there are lots of associations playing "catch up" because their dues have either been too low for too long, and/or for too long they've kicked capital improvement plans down the line. And while the rise in insurance premiums and taxes has caught every association off guard, those associations playing catch up have been disproportionately impacted. A great individual unit might warrant sufficient buyer interest, but that interest can completely evaporate if the association's financial health is poor.

Rules and Regs: Additionally, associations can deter buyers for reasons outside of their financial weakness. I'm referring to restrictive rules and regulations, specifically those that are restrictive in their pet and rental policy.

Seattleites love their dogs. Associations that don't allow dogs, expect a more difficult time in selling that unit and more time on the market. Associations that have weight policies on pets (25lbs and less) can also make it difficult, but at least offer something for dog owners. Cats seem to be acceptable everywhere. Pretty unanimously, most projects will have a 2 pet maximum. There's lots of variety when it comes to pets, just remember being excessively restrictive on dogs is not helpful in selling quickly.

Restrictive rental policies can also deter buyers. Generally homeowners like the flexibility of having the option to rent out their home if they move out, but aren't wanting to sell. Except, if the building has a restrictive rental cap policy in place, this can leave a homeowner in a real pickle. To be fair, I'm not aware or any condo building that doesn't have a rental cap policy in place so they're all restrictive to some degree. Most associations have a 25%-50% cap meaning no more than 25% or 50% of total units can be rented at one time. Some of the more challenging associations will have caps at 10% and it's not uncommon to hear of wait lists where there are homeowners waiting to rent out their unit when an opening becomes available. Imagine buying a unit in a low rental cap association and you get an unexpected job change. You can sell, but the market is really unfavorable, but you also can't rent the unit because there's a waiting list. What do you do? This is a real situation for many homeowners, unfortunately.

Non-warrantable: This is the term used to describe a condo association ineligible for conventional financing. In other words, Fannie Mae and Freddie Mac won't back any mortgages for these associations (of course, that means neither will the VA or FHA). Associations become non-warrantable for a variety of reasons. It could be financial (low reserves, special assessments in place or on the way) or something else like more than 50% of the units being rented, a single person owning more than 10% of the total units, the association being involved in litigation, etc.

The only options for owners selling a unit in non-warrantable buildings are either selling to a cash buyer or a buyer financing via a portfolio lender (a lender who doesn't sell to Fannie/Freddie). Washington Federal (WaFed) used to be the go to non-warrantable lender, but they exited mortgage lending in recent years. While there is a lender, somewhere, who can finance a non-warrantable condo, that stigma and limitations alone are likely to scare off a vast majority of buyers before they make it inside the unit.

Amenities: I'm not talking about a fancy gym, rooftop deck, pool, etc. I'm referring to basic amenities like in-unit washer/dryer and parking. Units not offering one, or both of these luxuries, are a much harder sell taking up more time on the market.

Given the above, I hope I've illustrated all the variables that come into focus when prepping a condo owner on the challenges they might face when preparing to list their unit for sale. The unfortunate part is that so much of this is outside the control of the homeowner. It's not as if we can just change a restrictive pet/rental policy, properly fund the associations reserve balance, or create parking where it previously never existed. Don't get me wrong, there's a buyer for any property at a certain price. The more challenges in place, the more the price needs to make up for those deficiencies.

Onto the stats: The median sale price for a Seattle condo for the month of October 2025 was $577,562. That is down .42% from last year and up MoM from $523,687. Inventory is up 12.9% YoY and the months of inventory dropped to 5.21 months from 5.45 in September. Absorption still remains at historically putrid levels though it was at the highest level since July.

Have an amazing Thanksgiving. Onward!

Stats, a 50 year mortgage, and layoffs. The GSHMU, November 2025

Welcome to another edition of the Greater Seattle Housing Market Update. As always, to skip straight to the stats, you can do so by clicking here. For more information not mentioned in the video, continue below!

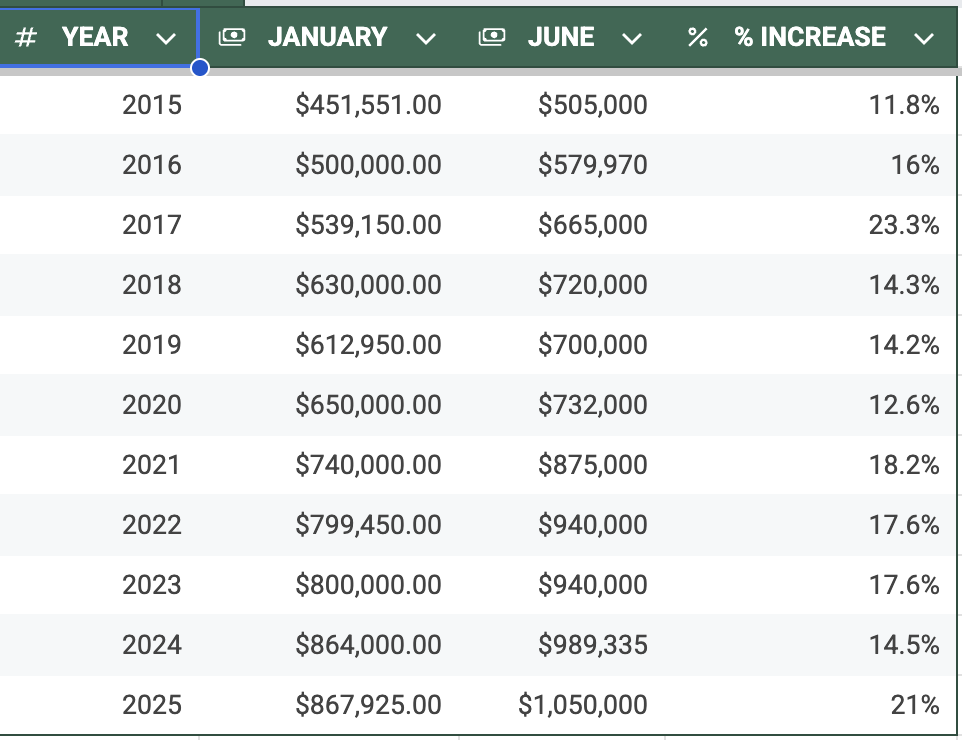

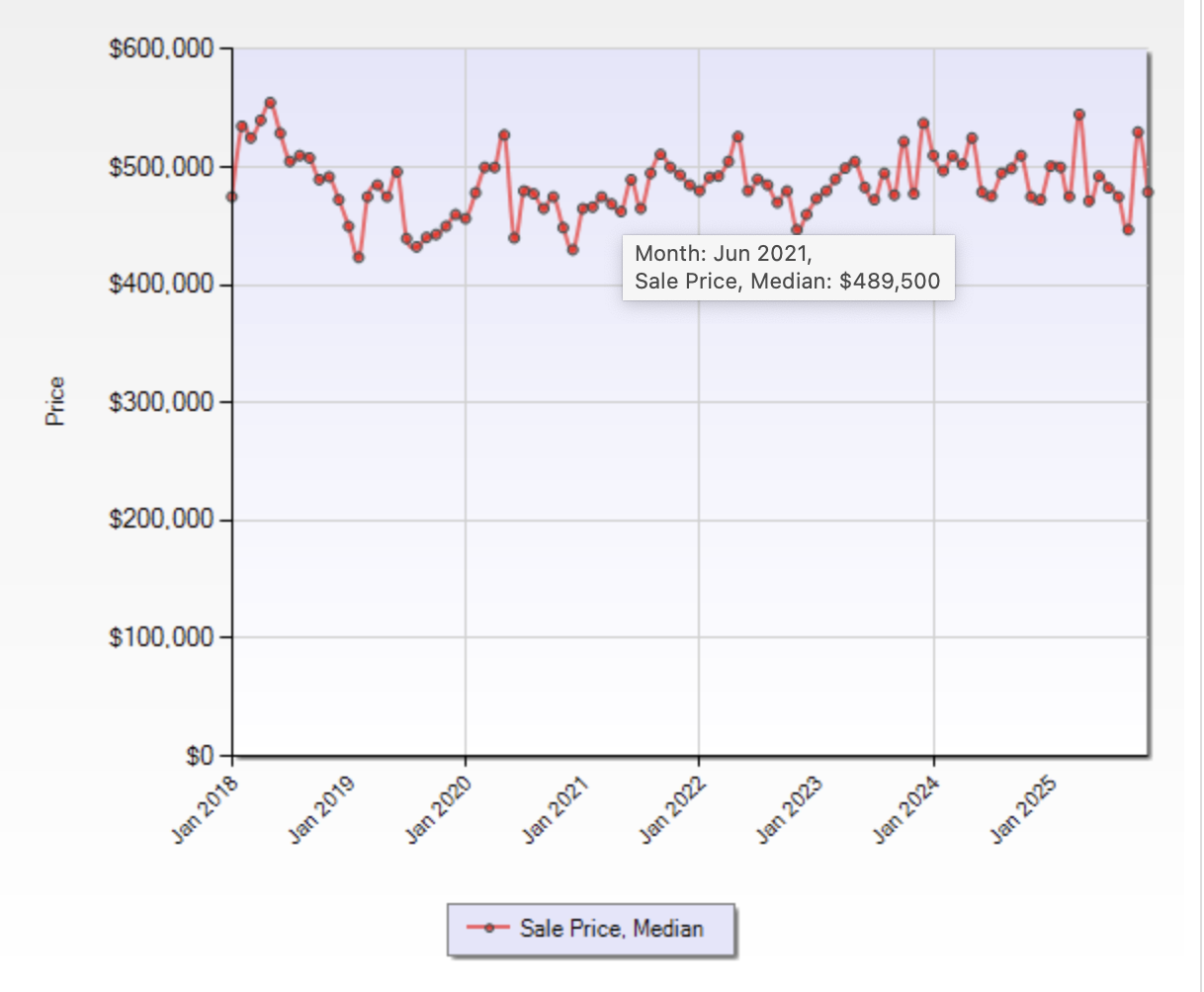

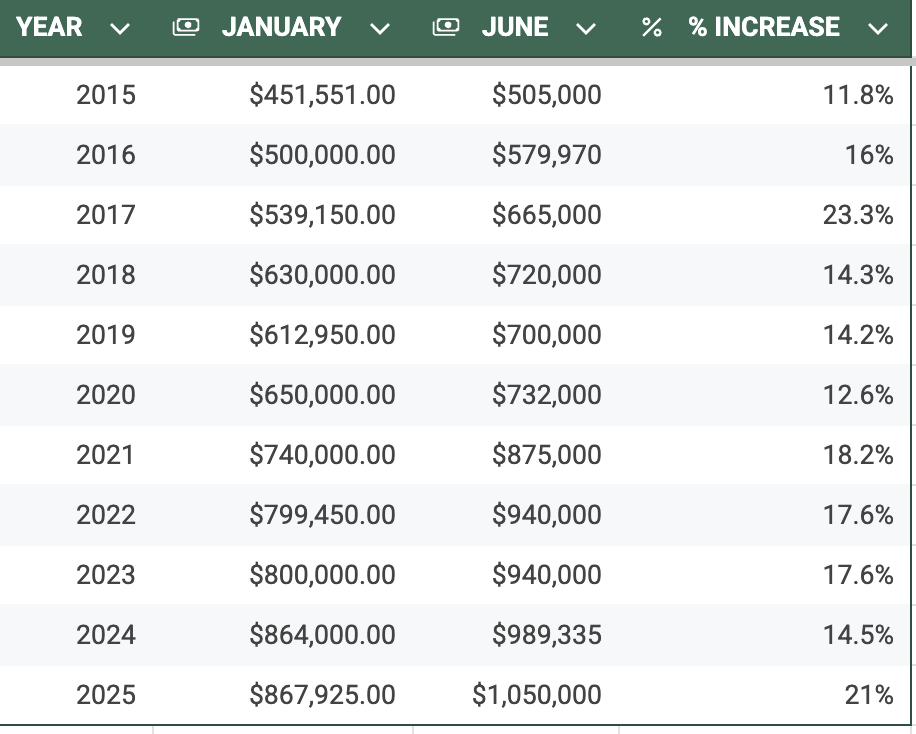

In past write ups, I've referenced seasonality in regard to inventory and buyer demand, but in this edition, I want to focus on Seattle home appreciation, specifically within the first 6 months of the year. Appreciation in our market almost takes place entirely within the first 6 months of every year. January is always the bottom point for the median sales price and then values gain, quite significantly, through the second quarter. In Q3 values stall a bit, and then at the end of the year they dip only to restart their upward trend a few months later once the new year turns over. See below the starting Seattle median sale price in January, June, and the percentage increase.

Below charts the relationship in a more viewer friendly version.

What does this mean? First, I'm never one to suggest "timing the market". It's about finding the right home, however long that might take. That being said, the sooner into the new year a buyer finds a home, the less, on average, they're paying. After being provided this information, buyers sometimes conclude that it's best to buy in Q3 or Q4 once values have stagnated or possibly even declined. There's no error in that thinking, but remember this; Pricing a home involves using data of recent sales. Setting a listing price for a home set to hit the market in Q1 means using data from similar sales that took place in Q4. Values decline at the end of the year, but buyer demand often pushes prices above their list price in Q1. On the other hand, Listing a home toward the end of the year involves using data from homes that sold when values were at their peak. 6+ months of appreciation leads to higher list prices. Even though demand isn't what it was earlier in the year and buyers might have leverage to buy the house under the asking price, that final sales price can still often be higher in August than what it would be in February. So just because the market conditions are more buyer friendly, that doesn't necessarily translate into getting the house any less expensive than what was possible earlier in the year despite more competition from other buyers.

Moving on. I'm sure you've heard that President Trump has floated the idea of creating a 50 year mortgage? If not, here's one of the many articles about this. Who knows how much bite there is to this idea, but I personally think it's a terrible idea.

It's true that a longer term mortgage would improve affordability, the benefit President Trump is touting, but that monthly savings would be negligible in the big picture. Don't forget, the longer the duration of the mortgage, the higher the interest rate. On an $800,000 loan, the 50 year option saves about $541/month, which is not insignificant, however the equity build up really slows down with a 50 year term. When you're paying so much in interest those first years, you don't start paying off significant amounts of principal until much later on in the amortization schedule compared to a 30 year alternative. In fact, over the life of the loan, the borrower taking out a 50 year mortgage ends up paying roughly $900,000 MORE in interest on this $800,000 example! See below:

Metric. 30-yr 50-yr Difference

Monthly Payment $5,096 $4,555 -$541

Total Interest $1,034,584 $1,932,989 + $898,405

I'm all for affordability, but not at the expense of equity. And certainly not at these proportions.

And finally, the elephant in the room, the recent layoff situation. First of all, I want to sympathize with those who have been impacted. My purpose isn't to diminish what any layoff might mean for their personal lives and situations. Instead, I'm going to attempt to offer a headline alternative away from the doom and gloom sensationalism. The below is an excerpt I pulled from a lender contact of mine, Kyle Bergquist of Cross Country Mortgage.

"...I do want to discuss what happened (recently) in the context of its potential impact on our Puget Sound Housing Market. Here’s the thing: The health of a local job market is absolutely imperative to the health of the local real estate market. Simply put: A strong job market drives demand for housing – it attracts new residents, and good wages can help a housing market gain value. With that said, we all know the inverse is also true – A bad job market is bad for housing. And if you were just rolling with the (recent) headlines, well, you’d think Seattle’s local economy was about to become a zombie graveyard.

Here’s the thing with corporate layoff headlines: Amazon HQ1 is here in Seattle (and HQ2 in Bellevue) so we immediately think doom and gloom when we see a headline stating 30,000 corporate layoffs. But did you know that Amazon has over 350,000 corporate employees worldwide?!? Only 64,000 of those corporate employees are here in Puget Sound (50,000 in Seattle, 14,000 in Bellevue). So obviously the number isn’t going to be 30,000 HERE in Puget Sound - It’s up to 30,000 worldwide…or 14,000 worldwide?... I don’t know what the actual number is anymore, but I do know it’s only 2,303 layoffs here in Puget Sound.

Again, really terrible for all those employees – I don’t want to take that away from them; BUT if we’re looking at this purely through the lens of how this might impact our local housing market, then it’s important to know that most employees who were affected will have 90 days to look for a new role internally. During that time, Amazon recruiting teams will be prioritizing internal candidates, and according to Amazon’s job board, there are currently 11,048 open jobs posted. Why doesn’t the media talk about that more?

The headlines we don’t get are how many people were hired in any given month. We get all the bad news, with very little good news."

While definitely unfortunate, I don't believe these layoffs are the fuse that's going to set off a firework of declining home values. Anecdotally, I have buyers experiencing massive competition for certain homes in certain areas well above $1,000,000. As I've (hopefully) made clear in past reports, property type and location are returning to paramount importance when buyers are home shopping.

Onto the stats:

Seattle: In October, the median sale price for a Seattle SFR was, $1,049,999. This is the second highest median sale price of all time! This was up 8% YoY and up MoM from $975,000. Inventory was up 21% YoY while the months of inventory decreased to 2.3 months from 3.08 in October. Watch for falling months of inventory over the next few months! Also interesting is that the absorption ratio registered the LOWEST figure ever recorded in the 6+ years I've been keeping track. Low absorption yet a 2nd all-time high sale price? It seems counterintuitive.

Eastside: The median sale price was $1,550,000. That is exactly the same it was a year ago and down slightly MoM from $1,575,000. Inventory is still up significantly at 76.4% more homes on the market, but the months of inventory reduced to 2.39 months from 2.79.

King County: The median sale price was $997,000. That is up 3.9% YoY and up MoM from $957,000. Inventory is up 33.1% YoY and the months of inventory decreased to 2.29 months from 2.76 the month prior.

Have an amazing Thanksgiving! Onward!

Seattle Condo Market Update — September 2025

Seattle condo prices hit a 2.5-year low in October as inventory stayed elevated and days on market stretched—giving buyers leverage before holiday listings tighten.

Happy Fall!

And welcome to the latest and greatest Seattle Condo Market Update. If you don't want to read and would rather watch, feel free to skip straight to the full YouTube video update here.

Good news and bad news for Seattle condo buyers

There was good news and bad news with September's stats for the Seattle condo market, depending on your perspective.

Ok, I'll give it a try. The good news is that sold inventory was up 45.2% YoY. 196 units sold in September of this year vs 135 units the month before. And YoY inventory is at its lowest mark (up 13.9%) year-to-date. In other words, inventory has been up YoY all year, it's just up at the smallest amount YTD.

However, the bad news is that the more sales resulted in lower sale prices. In fact, the median sale price for a Seattle condo in September registered the lowest amount ($523,687) since February of 2023. More sales, declining inventory, yet lower sales prices? Intuition would suggest the opposite, yet here we are. The optimist in me hopes this is the bottom and it's only up from here.

Why neighborhood matters for Seattle condo prices

Of course, the market is not a one-size-fits-all market. Geography plays a HUGE role in determining the expectations for sellers and I've reported A LOT on that in the past few months. For example, the months of inventory for Northwest Seattle (think Ballard, Greenwood, Green Lake, Fremont, Wallingford, etc) is 2.83 months. Contrast that to the Downtown/Belltown market of 6.71 months and you can see how important geography is.

Of course, the new construction backyard DADU's that you find in North Seattle don't exist in the downtown area so that also contributes to the vast difference since those are more desirable than units in high rise downtown buildings.

What inventory trends are telling us in 2025

Interestingly, over the last two years, and so far YTD, September has been the month of the year that's had the most inventory available. July is also well represented, too. We'll see if October can dethrone September.

Showing activity and what we’re seeing

Off topic, but something pretty cool that I just discovered. Our NWMLS has come out with a new tool tracking the amount of showings through the Supra keybox network. Granted, this data is across the entire NWMLS so there's no way for me to break this down into more microscopic data (county, cities, property types, ec), but it's interesting to see activity show exactly what we have been experiencing.

Despite more inventory growing during this time, showing activity decreases until after Labor Day, where it then picks up for two weeks, before declining again. But showing activity is up from last year, so that's good news (below). Again, not really tied to anything, I just found that interesting :)

Key Seattle condo stats for September 2025

Onto the stats:

The median sale price (as previously mentioned) for a Seattle condo in September 2025 was $523,687.

That is down 13.6% YoY and significantly down MoM from $595,000.

Inventory is up 13.9% YoY, and the months of inventory rose to 5.45 months from 5.18 the month prior.

Have an amazing Halloween. Onward!

Watch the full Seattle condo market update

Want more details? Watch my full Seattle condo market update video on YouTube for September 2025.

Seattle & Eastside Real Estate Market Update — September 2025

Seattle’s median slipped to $975K with inventory near 3 months, giving buyers more breathing room; the Eastside held around $1.58M—sellers should price and present strategically.

Welcome to October!

And welcome to the latest edition of The Greater Seattle Housing Market Update. As always, to skip the good stuff and go straight to the stats video, you can do so by clicking here. But for deeper reporting, continue reading below.

It's election season! At least it is in Seattle, where our mayoral election is set to take place next month. Incumbent Mayor Bruce Harrell is hoping to best challenger Katie Wilson and one of, if not the hottest issue on the minds of voters, is housing.

The shortage of housing, specifically affordable housing, is not an issue unique to Seattle. It's taking place all throughout the country. While politicians can, and will forever continue to offer solutions to this problem, I'm going to give you my wildly unpopular take. Brace yourself. Here it comes: And that is, housing is simply forever destined to be expensive in our region.

Before marching at me with pitchforks and torches, hear me out: while this is my opinion, it's shaped by some of the most trusted and influential sources when it comes to our regional housing market.

While attending a recent function with some of the region's best and brightest housing economists (Matthew Gardener and Mike Appleby), the fundamental dynamics of supply and demand, land use, and shifting population demographics were on major aspects of their presentation.

In as concise a summary as possible, the Greater Seattle area has more or less been entirely built out. That means any piece of developable land has already been developed to support a house. Note, that doesn't mean we've maximized the amount of houses we can build on every lot, but in other words, every lot that can feasibly contain a housing unit, already does. That's according to the last urban growth area plan that's now roughly 30 years old and hasn't been amended since. I won't get into all of that, but simply reshaping/rezoning some of those antiquated boundaries would open up more areas for future development. Back to the problem, there's really no developable land left.

Additionally, regardless of what does or doesn't get changed in the UGA, we've got a growing problem:

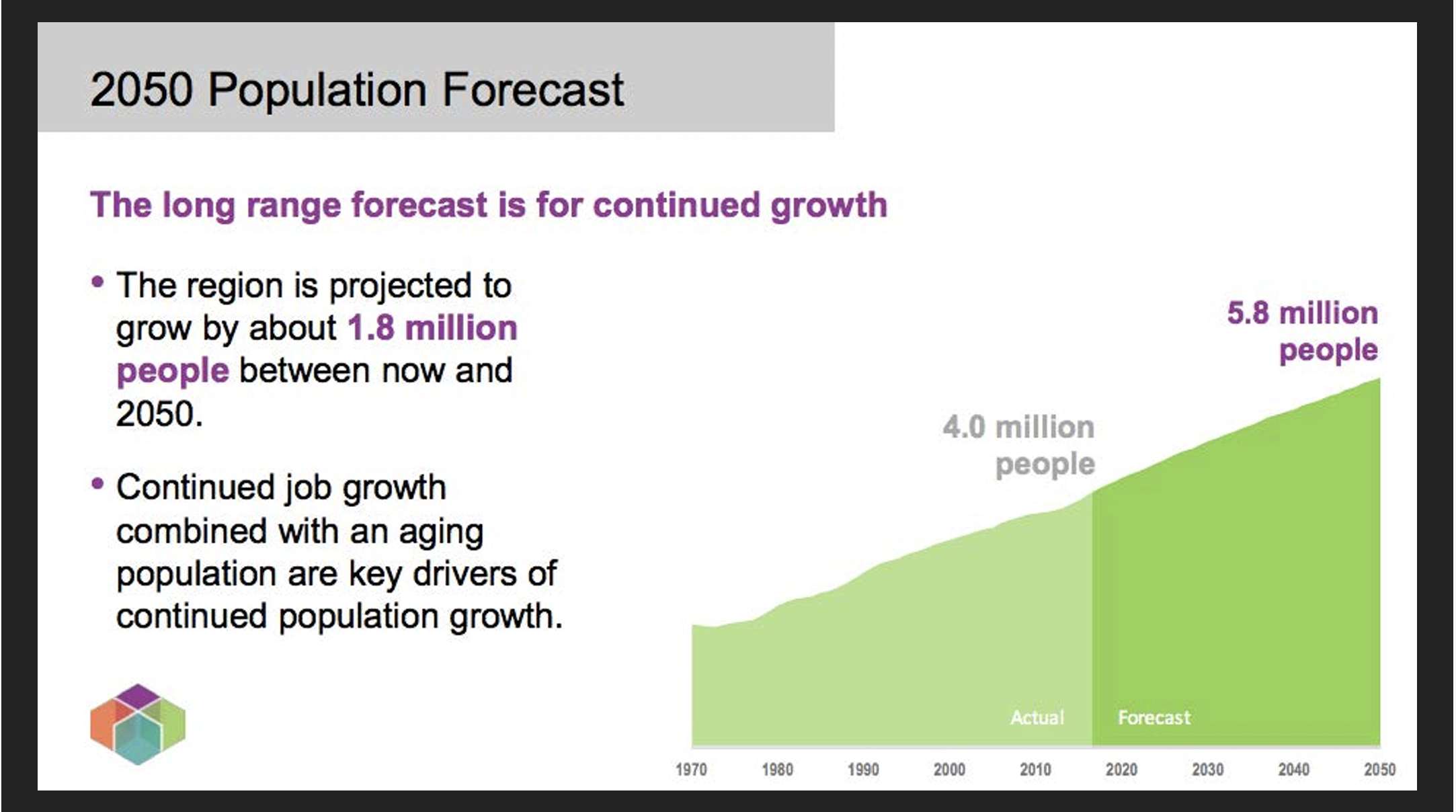

Our region (King, Snohomish, and Pierce counties) are estimated to add over 1,500,000 people in the next 25 years taking the region's total population to just under 3,000,000. See below how cities within King County are forecasted to increase.

We've established there's no developable land left PLUS it's evident we need to embrace for continued population increase. Not a great combo when it comes to hoping for lower housing costs. But that's not all...

Circling back to politics; housing is (and should be) a very hot button issue when it comes to our local elections. Given the above, we know there's really nothing politicians, developers, anybody outside a divine intervention can do because we can't create more land. Being surrounded by water, forrests, hills, etc is one of the many reasons we love living where we do. But it also means we're topographically handcuffed from being able to create housing. Contrast this to areas like Texas, Las Vegas, the midwest, etc where land is so plentiful and building so easy (and far less expensive). More on that below:

Home construction/development is built upon four pillars:

1) Acquisition cost

2) Labor

3) Materials

4) Regulatory costs

We already established housing in general is expensive because of limited supply. Even those teardown homes that can be bought and replaced with multiple homes or townhomes are not cheap because the land is so valuable. Developers are paying a lot just to acquire the land, even when adding more homes than the one they're buying to tear down.

In case you've been living in a bubble over the past decade plus, just about everything costs more here compared to the rest of the country. This includes labor and materials. Our cost of living is high, therefore labor is very high. Materials aren't cheap either.

Perhaps the most forgotten variable in the cost of housing are the regulatory costs. It's estimated that roughly 25% of the total cost of home building is set aside for permitting and regulations. That's simply absurd.

If you want to look at the one area of housing a politician could actually make a realistic promise to reduce costs for the consumer, it's in the permitting process. Yet this is a huge revenue source for governments so can we really expect them to be okay with decreasing these fees? I'm not holding my breath. That being said, I will throw praise in the direction of Mayor Harrell and others who have recently recognized and made efforts to streamline the regulatory processes, and costs, that go into building ADU's, DADU's, and condominium-ized homes in Seattle.

I've been saying this for a LONG time, but in regard to housing I think the extreme NIMBY's are overly concerned at what additional housing in their communities will do to their home values, just as I believe extreme YIMBY's are far too hopeful thinking these added units will be "affordable". Housing is simply destined to forever be very expensive in our area. Don't be fooled by empty statements or promises from local politicians.

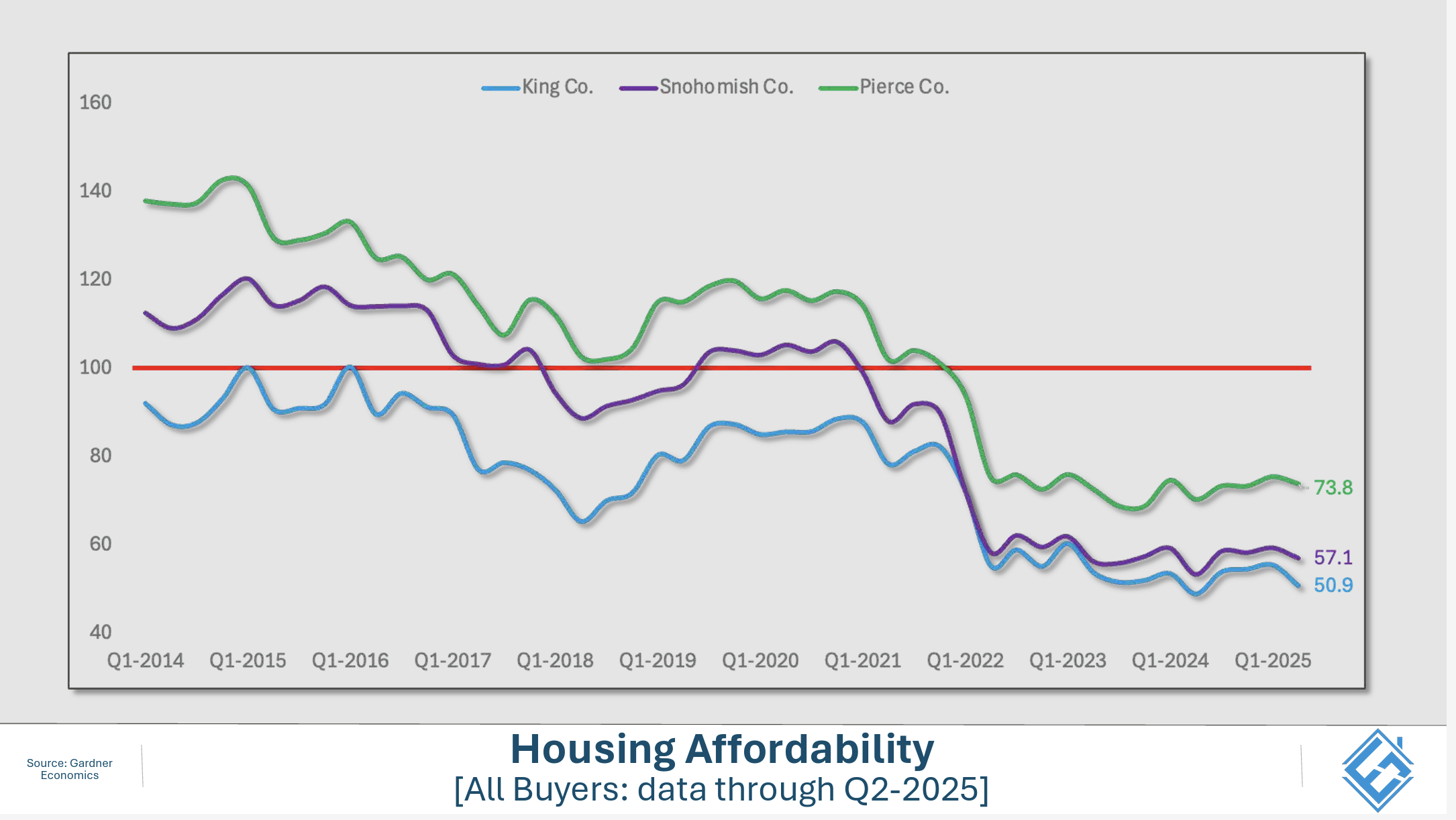

See overall affordability challenges below:

Onto the stats:

Seattle: September 2025 median sale price of $975,000. That is up 3.9% YoY, but down MoM from $1,000,000. Note, this was the first month since March that Seattle didn't notch a median sale price of $1m+. Inventory is up 12.1% YoY and the months of inventory increased to 3.08 months from 2.25, which is fairly significant.

Eastside: September 2025 median sale price of $1,575,000. That is up 3.1% YoY, and down MoM just $10,000. Inventory remains highly elevated at 60.3% more homes on the market YoY, yet the months of inventory increased only slightly to 2.79 months from 2.68 MoM.

King County: September 2025 median sale price of $957,000. That is up .7% YoY and down MoM from $990,000. Inventory is up 26.2% YoY and the months of inventory rose to 2.76 from 2.47 in August.

Have an amazing October! Onward!

Greater Seattle Housing Market Update — August 2025

Buyer activity hit multi-year lows, yet Seattle stayed a million-dollar city; the Eastside softened slightly and inventory is poised to tighten as we head into fall.

Welcome to the latest edition of the Greater Seattle Housing Market Update. As always, to skip the good stuff and go right to the latest figures for August, you can do so by clicking here. For more analysis, continue below!

This Seattle Times article was published on September 5th and it breaks down, very simplistically, the diverse real estate market that we're experiencing (bonus points if you noticed I'm quoted in this article). Perhaps more than ever since I've been a realtor, factors like location and property type are increasingly influential when factoring in time on market, and thus seller expectations. I've discussed this before in past market updates, but can't stress enough how important it is to paint finely as opposed to broadly when breaking down the local housing market.

I know the above isn't the prettiest, but bare with me. I want to include the connection between three variables: the median sale price, months of inventory, and median days to sell over the past 6+ years. What we see is a little different from what I would have expected.

Thinking back to our ECON 101 classes, we're reminded of the fundamental dynamics of supply and demand and I know nobody reading this is a stranger to the supply/demand relationship within housing. Especially over the last few years. But is the market cooling, or is it gaining strength? There are plenty of articles saying one thing or the other. So which is it?