If the Market Feels Sluggish, It's Not You. The GSHMR for February, 2026

Welcome to March Madness!

And welcome to the latest edition of the Greater Seattle Housing Market Review. As always, to skip the good stuff and go right to the stats, you can watch them via this link here. For more infotainment, continue reading below!

As the title suggests, if the start to 2026 has felt lethargic, you're not alone. January is never robust as the market is waking up from the holiday hangover, but by February the market turns from dormant to competitive with such quickness that it catches many buyers, and some realtors, flat footed. By March, the market feels like a runaway train. A lot of change in a short amount of time.

In last month's GSHMR I reported on the "dip" that takes place every January in regard to home values. In that report I predicted that once February's data is published we'll see the market "wake up", and whatever optimism might have been gained by reading January's stats will soon be decimated once February's stats become available. We saw exactly that. See below:

Seattle: The median sale price in February registered $962,500. That is down just .26% YoY, but up massively MoM from $850,000. Inventory remains elevated with 33.8% more homes on the market YoY, but the months of inventory, which was unusually very high in January, dropped significantly to 2.68 from 3.39.

Eastside: - The median sale price registered $1,566,782. That is down 7% YoY, but up MoM from $1,435,000. Inventory remains significantly higher at 57.8% more inventory YoY and the months of inventory actually increased slightly to 3.23 from 3.17 MoM.

King County - The median sale price registered $936,000. That is up 2.3% YoY and up MoM from $850,000. Inventory remains significantly elevated at 42.4% more inventory YoY, but the months of inventory dropped to 2.71 from 2.92.

In addition to the supply/demand dynamics, there are also a number of macro, geopolitical issues going on right now that have the potential to influence the local housing market.

War in Iran- Obviously there are numerous consequences of a global conflict such as this one, but to be succinct I'll focus on the impact the conflict has had on mortgage rates. Historically, global conflicts are actually favorable for lower mortgage rates because of the "flight to safety" that exists when investors sell off equities/stocks and buy treasuries/bonds, the safer, less risky asset. The demand for bonds pushes mortgage rates lower. However, so far in this conflict, that has NOT been the result.

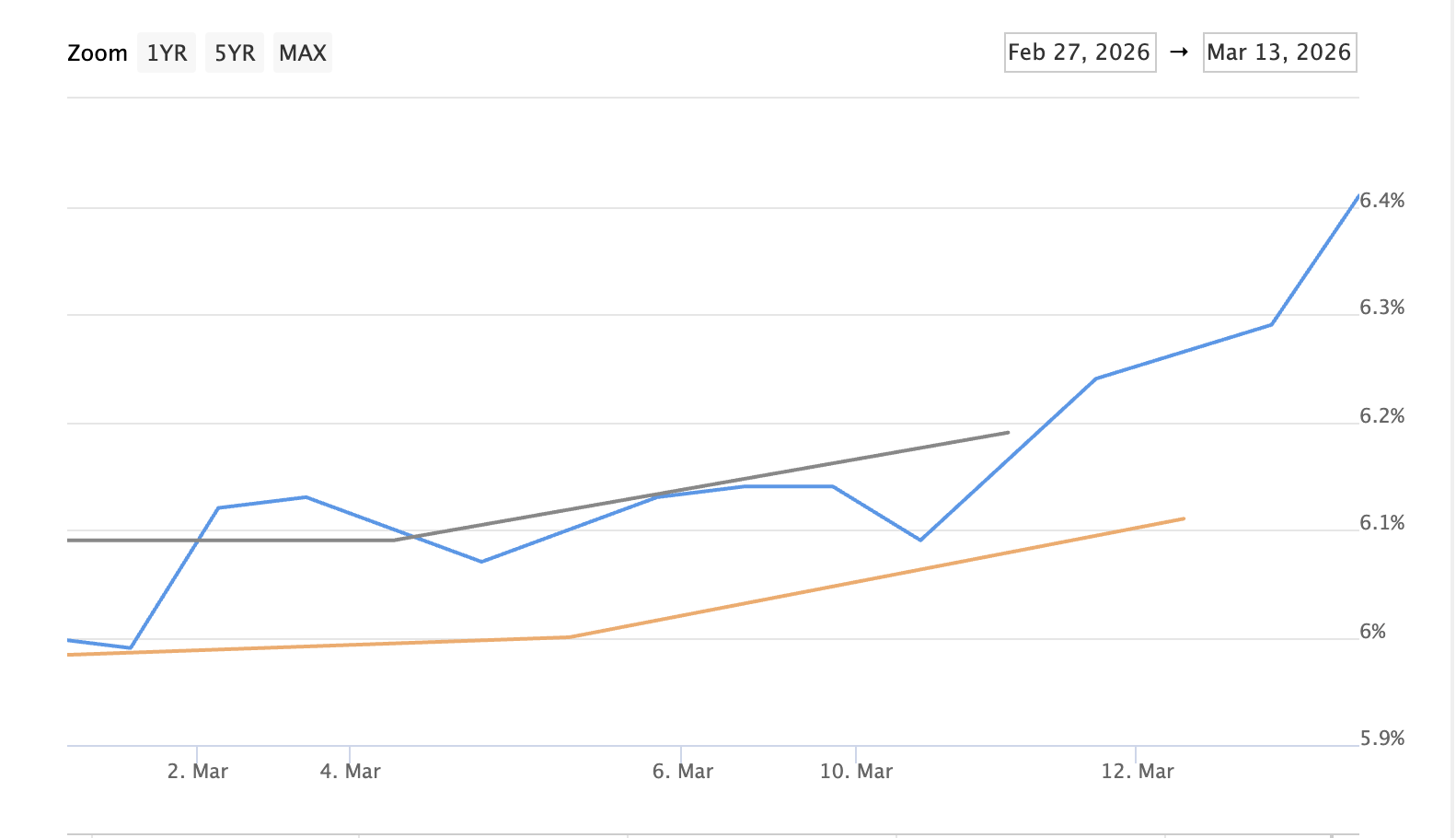

Why? Oil. Because of Iran's prominence in the global oil trade, disrupting the production and distribution of a commodity as valuable as oil is bad for inflation (just see how much the cost of oil, and gas, has risen during this active conflict). Inflation is not good for mortgage rates so despite a military conflict that is historically favorable for mortgage rates, interest rates have actually increased during this conflict. How much longer this conflict continues, and how much higher rates can potentially move, remains to be seen. See below how rates have trended from February 27th through March 13th. Rates are about .375%-.500% higher.

The labor market - This isn't specific to just 2026, but local layoffs continue to be a news headline. Of course, like any headline (or even article these days) we have to question is the reporting fact based, or based out of marketing (selling clicks)? There's some truth to both angles there, but whether based in fact or rhetoric, if someone fears their job/income isn't as stable as they prefer, that can definitely shut down their pursuit of homebuying.

"Millionaire Tax" - Washington State is getting close to an income tax applying to those making over $1,000,000/year. Even if this passes, it will be fought in courts and that will likely take time so I don't see this impacting our market any time soon, if ever. Back to the media and their need for clicks, articles like this one are detailing certain wealthy individuals, like Starbucks CEO Howard Schultz, who have already vacated to more tax friendly states. Could this impact the ultra luxury market? Perhaps, but very unlikely to cause any ripple effect from there.

However, if we see more indigenous companies like Starbucks, who just shifted corporate jobs to Tennessee, follow their lead, that can become problematic. And heck, even the Seahawks general manager said that a potential income tax could make free agent signings more difficult in attracting top talent. Don't mess with our Seahawks!!

Have an amazing March. Onward!